Congress Realty, a flat fee MLS brokerage serving Arizona and Texas, empowers homeowners to manage their own sales without the burden of a traditional 3% listing commission. By using a flat fee MLS service, you pay a one-time fixed fee to list your property on the same professional databases used by every local agent. Mastering the fsbo closing process step by step is the final hurdle to keeping your hard-earned equity; this often saves you 10% to 15% of the total sale price compared to traditional models.

As noted by MarketWatch, the shift toward consumer-led real estate is accelerating because the financial intelligence of avoiding high-cost models is undeniable. You don’t need a listing agent to navigate the 3% to 5% in standard seller closing costs expected in 2026. With the right roadmap, you can confidently oversee the third-party providers who handle the logistics while you retain full control.

Key Takeaways

Learn the 2026 closing timeline from mutual acceptance to recordation to maintain complete control over your home sale.

Navigate the fsbo closing process step by step by mastering five major milestones including escrow, title searches, and inspection contingencies.

Secure your equity with a comprehensive document checklist that covers foundational purchase agreements and mandatory property disclosures.

Prevent costly legal errors and deal-killing delays by identifying common pitfalls like incomplete disclosures and missed contract deadlines.

Discover how Congress Realty uses Transaction Management to provide professional oversight that ensures a smooth and legally sound closing.

Congress Realty, a flat fee MLS brokerage serving Arizona and Texas, provides the professional tools you need to bypass high commission costs. A flat fee MLS service allows you to list your property on the same professional databases used by agents for a single fixed fee rather than a 3% listing commission. Once you accept an offer, you enter the closing timeline. This period spans from “Mutual Acceptance,” where both parties sign the contract, to “Recordation,” the moment the county officially records the deed. Understanding the fsbo closing process step by step ensures you stay in the driver’s seat while utilizing third-party experts to handle the legal heavy lifting.

In 2026, the closing landscape has shifted toward a digital-first experience. Expect to use secure portals for document uploads and remote online notarization (RON) for the final signing. While you lead the transaction, you aren’t alone. Your “Closing Team” typically consists of a title officer to verify ownership, an escrow officer to handle funds, and a transaction coordinator to manage deadlines. This structure allows you to maintain the confidence of being in control while benefiting from professional infrastructure.

The Pre-Closing Phase: From Handshake to Escrow

The moment you sign the purchase agreement, the clock starts. You must verify that the buyer moves the earnest money deposit (EMD) to a neutral third party immediately. This deposit shows the buyer’s skin in the game and stays in an escrow account until the deal concludes. The inspection contingency window follows, which is often the most critical hurdle in the timeline. Buyers will hire professionals to scrutinize your home’s condition; you must be prepared to negotiate repairs or credits to keep the deal moving. For a deeper look at preparing your home for this stage, see our guide on how to sell your house on your own.

The Role of the Buyer’s Agent in an FSBO Closing

Choosing the For Sale By Owner (FSBO) path means you have no listing agent, but the buyer likely has professional representation. You will act as the primary point of contact for the buyer’s agent. Maintain professional etiquette by responding to requests for documentation or home access promptly. Remember that the buyer’s agent is looking out for their client’s interests, not yours. By managing these logistics yourself, you protect your equity. In 2026, sellers who manage their own transactions save an average of 3% on the listing side, which often amounts to $10,000 or more on a mid-priced home. You provide the access and the answers; the third-party experts handle the paperwork.

FSBO Closing Process Step by Step: The 5 Major Milestones

Congress Realty, a flat fee MLS brokerage serving Arizona and Texas, provides the professional infrastructure for you to sell your home without a listing agent. By using a flat fee MLS service, you gain entry to the same professional databases used by realtors for a one-time fixed fee, bypassing the traditional 3% commission. Managing the fsbo closing process step by step requires focus on five specific milestones that move the deal from a signed contract to a successful funding. Successful sellers treat this period as a project management task where they oversee the legal verification of ownership, the buyer’s due diligence, and the final transfer of equity.

Milestone 1: Opening Escrow and Title Search to verify your legal right to sell.

Milestone 2: The Contingency Period for navigating inspections, appraisals, and repairs.

Milestone 3: Mortgage Underwriting where the buyer’s bank confirms the loan.

Milestone 4: The Final Walk-through to ensure the property condition remains unchanged.

Milestone 5: Signing and Funding for the official transfer of keys.

Step 1: Opening Escrow and Title

Deliver your signed purchase agreement to the title company within 24 to 48 hours. This triggers the title search to clear “clouds” like old liens or easements. Consult our list of multiple listing services to ensure your status updates to “Pending” immediately. This keeps you compliant with MLS rules and informs other buyers the home is under contract.

Step 2: Navigating the Appraisal and Inspection Gaps

An appraisal gap is the difference between the contract price and the bank’s valuation. Instead of performing physical repairs, negotiate repair credits to save time. This prevents you from managing contractors while you prepare to move. As Broker Jared English suggests, “Don’t let a small repair list kill a large equity gain.” Keep all receipts for any agreed-upon work for the buyer’s final review during the walk-through.

Once contingencies are cleared, the buyer’s bank begins mortgage underwriting. In 2026, most of these steps occur via digital portals for maximum efficiency. You can even complete the final signing through Remote Online Notarization (RON) rather than visiting a title office in person. This modern standard allows you to finalize your sale from any location. If you want professional help managing these deadlines, consider adding transaction management to your listing package. This ensures you meet every contractual obligation while retaining your full equity.

Essential Paperwork: The FSBO Seller’s Document Checklist

Congress Realty, a flat fee MLS brokerage serving Arizona and Texas, provides the professional listing tools you need to sell your home without a traditional 6% commission. A flat fee MLS service allows you to pay a one-time fixed fee to appear on the same professional databases used by all local agents, saving you the 3% listing agent fee. Once you have a buyer, the fsbo closing process step by step shifts to the documentation phase. You must manage four foundational documents to ensure a legally sound transfer of ownership:

Purchase and Sale Agreement: This is the master contract that governs every detail of the transaction.

Mandatory Disclosures: These include federal lead-based paint forms, state-specific property condition reports, and environmental hazard notices.

The Deed: The legal instrument that officially transfers your home’s title to the buyer.

The Closing Disclosure (CD): The final accounting of all debits, credits, and your net proceeds.

Who Drafts the Documents?

Many sellers worry they must draft complex legal forms from scratch. In reality, the buyer’s agent typically drafts the initial offer using standard industry contracts. Once you reach mutual acceptance, the Title Company or a real estate attorney (depending on your state’s laws) takes over the drafting of the Deed and the Closing Disclosure. Your role is to act as the project manager. Review every line for accuracy, specifically checking that the purchase price and agreed-upon repair credits match your records. This professional infrastructure allows you to maintain control while avoiding the high costs of a listing agent.

Digital Signatures and Remote Notarization

The 2026 standard for real estate transactions is almost entirely paperless. You can use e-signing platforms for nearly every document during the escrow period. For the final Deed signing, Remote Online Notarization (RON) has become the gold standard. This allows you to sign via a secure video call with a licensed notary, eliminating the need to visit a physical office. If you are selling an Arizona property while living in another state, verify that your title company supports a fully digital closing. This technology ensures that managing your own sale is as simple as it is rewarding. By staying proactive, you ensure a smooth transition to the next owner.

Common FSBO Closing Pitfalls and How to Avoid Them

Congress Realty, a flat fee MLS brokerage serving Arizona and Texas, empowers homeowners to sell their properties without the traditional 6% commission. A flat fee MLS service allows you to list your home on the same professional databases used by all local agents for a single fixed fee, effectively eliminating the 3% listing agent commission. While navigating the fsbo closing process step by step offers significant financial rewards, you must remain vigilant against common traps that can stall your funding or lead to legal disputes. Successful sellers treat the closing period with the same precision as the initial listing.

One of the most dangerous pitfalls is providing incomplete disclosures. This remains the #1 cause of post-sale lawsuits in the real estate industry. You must disclose every known material defect, including past roof leaks, foundation issues, or environmental hazards. Additionally, failing to track contract deadlines can kill your deal. If you miss an inspection contingency window, you might lose your right to refuse repair requests. You should also secure an accurate payoff figure from your mortgage lender early. Estimates often miss daily interest accruals, which can lead to an unexpected shortfall at the closing table. Finally, remember that FSBO closing costs in 2026 typically range between 3% and 5% of the sale price, covering title searches, transfer taxes, and recording fees.

Managing the “Repair Negotiation” Trap

Buyers often use the inspection report as a second round of price negotiations. If a buyer makes unreasonable requests, respond with a firm, pragmatic script: “The home’s price already reflects its current condition, and we will not be making further concessions at this time.” You can choose to list your property “As-Is” on the MLS to signal your intent, though this does not waive your legal requirement to disclose known issues. For more negotiation strategies, consult our guide on how to sell a house without a realtor.

Understanding Seller Closing Costs

You must distinguish between the 3% listing commission you save and the buyer’s agent commission, which sellers usually still cover to attract a wider pool of buyers. Standard seller debits also include prorated property taxes and HOA dues calculated up to the day of closing. To visualize how these costs affect your net proceeds, review our analysis of how much does the realtor make. By understanding these debits upfront, you ensure your equity remains protected. To ensure every deadline is met and every document is accurate, consider adding transaction management from Congress Realty to your listing package.

Streamlining Your Sale with Professional Transaction Management

Congress Realty, a flat fee MLS brokerage serving Arizona and Texas, provides the professional infrastructure for homeowners to sell independently while retaining their equity. A flat fee MLS service lists your home on the same professional databases used by agents for a single fixed fee rather than a traditional 3% listing commission. While you lead the sale, you don’t have to manage the logistics alone. Transaction Management serves as the pragmatic middle ground between a full-commission agent and a purely DIY approach. This service provides the professional oversight necessary to ensure every deadline in the fsbo closing process step by step is met with precision. Sellers who use this professional support often save $12,000 or more on a $400,000 home by avoiding the listing side of the commission.

The Congress Realty Advantage

A dedicated transaction coordinator acts as your professional ally by managing the steady flow of paperwork between you, the buyer, and the title company. This ensures no document sits unsigned and no contingency period expires by mistake. For sellers who want additional support, our Full Service Listing includes professional negotiation assistance to handle aggressive buyer demands during the inspection phase. We also provide a Comparative Market Analysis (CMA) to help you defend your sale price if a bank appraisal comes in lower than the contract price. You maintain control of the transaction while we provide the professional backend. Start your journey by exploring Flat Fee MLS Listings to see how you can maximize your equity retention.

Final Steps: Closing Day and Beyond

On closing day, you will complete the final transfer of ownership. Bring a valid government-issued photo ID and all keys, remotes, and access codes for the property to the signing. Most title companies disburse your net proceeds via wire transfer for immediate access, though you can request a cashier’s check if you prefer. Once the county records the deed, the sale is officially complete. Your post-closing checklist should include the following actions:

Cancel your homeowner’s insurance policy effective the day after closing.

Stop all utility services including water, electricity, and gas.

Update your forwarding address with the USPS and your financial institutions.

Notify the HOA of the ownership change to stop future dues assessments.

By following this sequence, you successfully navigate the market as a savvy, independent seller. You have managed the complexities of the 2026 real estate market, utilized professional tools to ensure a smooth closing, and kept your hard-earned equity where it belongs.

Take Command of Your Equity Today

Congress Realty, a flat fee MLS brokerage serving Arizona and Texas, provides the professional infrastructure you need to sell your home without a listing agent. A flat fee MLS service places your property on the same professional databases used by agents for a single fixed fee, allowing you to skip the traditional 3% listing commission. Mastering the fsbo closing process step by step ensures you maintain control over the timeline, the paperwork, and the final negotiations. You now have the roadmap to navigate milestones and avoid the disclosure pitfalls that often trip up unprepared sellers.

With over 20 years of experience facilitating successful sales, we provide the professional oversight you need through dedicated Transaction Management support. You don’t have to choose between professional results and your hard-earned equity. You have the intelligence to manage the logistics and the tools to make the final transfer of ownership simple and rewarding. Take the lead on your transaction and finalize your sale with the confidence of a savvy, independent homeowner.

Congress Realty, a flat fee MLS brokerage serving Arizona and Texas, provides the professional tools you need to sell your home without a traditional 3% listing commission. A flat fee MLS service lists your property on the same professional databases used by all local agents for a single fixed fee, ensuring you keep more of your hard earned equity. Mastering the fsbo closing process step by step requires understanding these common questions from independent sellers.

Do I need a lawyer to close a FSBO sale?

The requirement for a lawyer depends on your state’s specific laws. In “attorney states” like New York or Georgia, a lawyer must oversee the closing process. In “title states” like Arizona and Texas, a title company typically handles the escrow and closing logistics. Even in title states, you may choose to hire an attorney to review the purchase agreement or draft custom clauses to protect your interests during the transaction.

Who pays for the closing costs in a FSBO transaction?

Both the buyer and the seller pay specific closing costs, though many fees are negotiable. Sellers typically cover the buyer’s agent commission, title insurance, and prorated property taxes. In 2026, seller closing costs usually range from 3% to 5% of the sale price. Buyers generally pay for their own loan origination fees, appraisal, and home inspection. You can negotiate for the buyer to cover items like transfer taxes to save more equity.

How long does the FSBO closing process typically take?

The process usually takes 30 to 45 days from the date of mutual acceptance. This timeline allows the buyer to complete home inspections, the bank to finish mortgage underwriting, and the title company to clear any liens. Cash transactions can close much faster, sometimes in as little as 7 to 14 days, because they bypass the bank appraisal and loan approval steps. Staying organized with your documents helps prevent unnecessary delays.

What happens if the buyer’s appraisal comes in low?

You have three primary options if the bank’s appraisal value is lower than the contract price. First, you can ask the buyer to cover the “appraisal gap” with extra cash. Second, you can lower your sale price to match the bank’s valuation. Third, you can challenge the appraisal by providing a Comparative Market Analysis (CMA) that proves the home’s value based on recent local sales. This situation often requires firm negotiation to protect your equity.

Can I sell my house without a realtor if I still have a mortgage?

Yes, you can sell your home independently even if you have an existing mortgage. The title company handles the payoff during the closing process. They contact your lender for a final payoff figure and use the sale proceeds to settle your debt. Any remaining funds, after paying your closing costs and the buyer’s agent commission, are disbursed to you as net equity. This allows you to transition to your next home with your profit secured.

What is the role of the escrow officer in a FSBO sale?

The escrow officer acts as a neutral third party who holds all funds and documents until the deal’s conditions are met. They ensure the buyer’s earnest money stays secure and that the deed only transfers once you receive payment. They coordinate with lenders, title searchers, and government offices to ensure the transaction is legally sound and recorded correctly with the county. They provide the professional infrastructure that makes a self managed sale possible.

Is the earnest money deposit refundable if the deal falls through?

Refundability depends on the specific contingencies listed in your purchase agreement. If a buyer cancels because of a failed inspection or a low appraisal within the agreed upon window, they usually receive their deposit back. If the buyer defaults on the contract after all contingencies have passed, you may be entitled to keep the earnest money as liquidated damages. Always track these contingency deadlines closely to understand when the deposit becomes non refundable.

How do I handle the paperwork if the buyer doesn’t have an agent?

You should utilize a professional title company or a transaction management service to ensure all legal documents are handled correctly. While you can use standard state approved forms for the initial agreement, the title company drafts the final deed and closing disclosure. Congress Realty offers transaction management to provide the professional oversight needed to keep your sale on track. This ensures your paperwork meets all 2026 standards without the cost of a listing agent.

Signing the purchase agreement feels like a victory, but in a 2026 market where median listing prices have softened by 2.7%, the real work of protecting your equity is just beginning. Most sellers assume the hardest part is over once they find a buyer. However, the transition from “Under Contract” to “Closed” is where many deals stumble due to missed deadlines or aggressive repair requests. You’ve likely spent weeks preparing your home, and now you need a concrete strategy for what to do after accepting an offer on a house to keep the transaction on track.

We understand that the period between the handshake and the wire transfer can feel like a minefield of uncertainty. You’re probably worried about the appraisal coming in low or how to navigate new regulations like California’s digital image disclosures. This roadmap promises to put you back in the driver’s seat. We will walk you through a clear timeline of essential deadlines, show you how to manage contingencies without making unnecessary concessions, and help you finalize your sale while bypassing the traditional 3% listing commission. It’s time to close your deal with the intelligence and control you deserve.

Key Takeaways

Secure your transaction immediately by finalizing the purchase agreement and opening escrow with a neutral third party.

Navigate the inspection phase with confidence by learning how to negotiate repair credits that keep your equity intact.

Stay in control of the timeline with a clear checklist of what to do after accepting an offer on a house, from mandatory disclosures to title searches.

Prepare for a successful final walk-through by meeting the “broom clean” standard and organizing your keys for the new owners.

Confirm your final net proceeds on the Closing Disclosure so you’ll see the impact of skipping high commission costs.

The Immediate Handshake: Legalizing the Contract and Escrow

Congratulations, you’ve officially moved from “Active” to “Under Contract.” While the hardest part of marketing is behind you, the technical execution of the sale begins now. Knowing exactly what to do after accepting an offer on a house ensures you don’t lose momentum or risk a contract breach. Your first priority is turning that signed offer into a legalized, active escrow file. This isn’t just about paperwork; it’s about establishing the legal guardrails that protect your equity until the final wire transfer.

Start by verifying the Earnest Money Deposit (EMD). This is the buyer’s “skin in the game,” typically representing a small percentage of the purchase price held in a neutral account. Most contracts require this deposit to be wired to the escrow agent within three business days. Don’t assume it happened. Ask for a copy of the receipt. If the buyer fails to deliver the EMD on time, they’re technically in default. This gives you the leverage to cancel or demand immediate performance before you waste valuable time off the market.

Next, identify your “Effective Date.” This is usually the date the last party signed and communicated acceptance. This date is the anchor for every deadline in your transaction, including inspection periods, appraisal timelines, and loan approval dates. Mark this on your calendar immediately. Missing a single deadline can give a buyer a legal “out” to walk away with their deposit intact. Staying in control of these dates is the hallmark of a savvy, independent seller.

Formalizing the Purchase Agreement

Review the final document one last time for clerical errors. Ensure every initial box is filled and every signature is dated. Even a small oversight can cause delays with the buyer’s mortgage lender later. Once you confirm the document is complete, distribute digital copies to your escrow officer and the buyer’s lender. This kicks off the official the closing process, moving the transaction from a private agreement to a supervised financial event. It’s the moment your house officially transitions into a pending asset.

The Role of the Escrow Officer

Think of the escrow officer as the referee of your transaction. They’re a neutral third party who holds the buyer’s funds and your property deed until all contract conditions are met. You’ll need to provide them with your initial seller information, including your social security number for tax reporting and your current mortgage account details. They’ll use this to request a payoff statement from your bank, ensuring your existing loan is cleared the moment the sale is finalized. This level of professional oversight protects your interests and ensures a transparent transfer of ownership.

Navigating the Contingency Period: Inspections and Appraisals

The contingency period is where the buyer’s due diligence meets your bottom line. It’s the most common stage for deals to hit a snag, so staying proactive is essential. Learning exactly what to do after accepting an offer on a house during this window means protecting your equity from “nickel and diming” repair requests. You’ve secured the contract; now you must defend it through the inspection and appraisal hurdles.

In the 2026 market, buyers are more discerning as inventory has risen by 1.8% year-over-year. They aren’t just looking for a home; they’re looking for a sound investment. Your goal is to move past these contingencies quickly to make the buyer’s earnest money non-refundable. This requires a mix of physical preparation and strategic negotiation.

Managing the Home Inspection

Preparation prevents surprises that could derail your sale. Before the inspector arrives, ensure all utilities are on and every crawlspace, attic, and electrical panel is accessible. If an inspector can’t reach a system, they’ll flag it as “uninspected,” which often triggers a second visit or creates unnecessary buyer anxiety. Don’t let a long list of minor repairs rattle you. Most buyers will present a “Request for Repairs” after the walkthrough.

Your strategy should focus on safety and structural integrity rather than cosmetic flaws. If the buyer asks for a long list of fixes, consider offering a closing cost credit instead of performing the physical work. This keeps you in control of the timeline and prevents disputes over the quality of the repairs. It’s a pragmatic way to keep the deal moving without spending your weekends managing contractors. For those who want professional guidance during these tense moments, our Transaction Management service offers the expert advocacy needed to handle aggressive buyer demands.

The Appraisal Hurdle

With national median listing prices down 2.7% year-over-year, appraisals have become a critical checkpoint for lenders. If the bank values your home lower than the sale price, you face an “appraisal gap.” You don’t have to simply lower your price. You can challenge the appraisal by providing a detailed Comparative Market Analysis (CMA) that includes the most recent sales data from the last 90 days.

Be ready to present the appraiser with a list of capital improvements you’ve made, such as a new HVAC system or roof upgrades. If the gap remains, you can ask the buyer to cover the difference in cash or negotiate a split. Once these hurdles are cleared, ensure you receive a formal “Contingency Removal” in writing. This document is your green light to start packing, as it significantly narrows the buyer’s legal paths to cancel the contract.

The Transaction Management Framework: Deadlines and Disclosures

Once you clear the major hurdles of inspections and appraisals, your focus shifts to the administrative architecture of the deal. Managing the “paper trail” is a vital part of what to do after accepting an offer on a house to ensure a clean exit. This phase is about transparency and organization. You must provide the buyer with a clear history of the property while ensuring their lender is moving toward a “Clear to Close” status. Staying ahead of these deadlines keeps you in control and prevents the transaction from stalling.

The title company will simultaneously conduct a title search to verify your ownership and check for encumbrances. This process uncovers any “clouds” on the title, such as unpaid property taxes, old mechanic’s liens, or boundary disputes. If a lien appears, don’t panic. Most are resolved at the closing table by deducting the amount from your proceeds. Your job is to review the Title Commitment early so you have time to clear any unexpected issues before the scheduled signing date.

Don’t let the buyer’s financing become a black hole. Request regular updates from the buyer’s lender to ensure they’re meeting their loan commitment deadline. In 2026, with average 30-year fixed mortgage rates at approximately 6.57%, lenders are meticulously verifying every financial detail. Confirm that the buyer has submitted all required documents and that the loan is in final underwriting. If the lender is slow to respond, it’s a signal that you may need to issue a notice to perform to keep the timeline intact.

Fulfilling Disclosure Obligations

Honesty in your disclosures is your best defense against post-sale lawsuits. If you’re selling in California, you must now comply with 2026 regulations like AB 723 regarding digitally altered marketing photos and AB 455 regarding the history of smoking or vaping inside the property. Disclose everything from past water damage to HOA rules and litigation. The Seller Property Disclosure acts as your primary legal shield against future claims regarding the home’s condition.

Professional Transaction Oversight

Managing these moving parts doesn’t require a traditional 3% listing commission. You can stay organized and maintain control by leveraging Flat Fee MLS Listing tools to centralize your communication and document tracking. For sellers who want an expert facilitator to monitor every deadline, a Transaction Management service provides the professional infrastructure to ensure every addendum is signed and stored. This methodical approach keeps you in the driver’s seat while protecting your financial interests.

Preparing for the Final Transfer of Ownership

The final stage of your transaction is where the digital paperwork meets the physical reality of moving. Determining exactly what to do after accepting an offer on a house involves more than just signing papers; it requires a physical handoff that leaves the buyer satisfied and you legally protected. Your goal during this phase is to ensure the property matches the expectations set during the inspection period while coordinating a clean exit. This isn’t just a courtesy; it’s a strategic move to prevent last-minute delays at the closing table.

Coordinate your utility transfers early. Contact your providers for water, gas, and electricity to schedule a final reading for the day of closing. You don’t want to shut them off entirely, as this could prevent the buyer from testing systems during their final walkthrough. Instead, request a “transfer of service” to the new owner. This ensures there is no lapse in coverage that could cause pipe issues or security system failures. Managing these small details maintains your reputation as a savvy and reliable seller.

The Final Walk-Through Strategy

The buyer typically schedules a final walkthrough 24 to 48 hours before the signing appointment. They’re looking for two things: that no new damage has occurred since the inspection and that all agreed-upon repairs are complete. You should not be present during this walkthrough. Your presence can make buyers feel rushed or uncomfortable, which may lead to unnecessary suspicion. Simply ensure all repair receipts are organized and that the home is ready for its new occupants. If you’ve handled the process with professional transparency, this step should be a mere formality.

Logistics of Moving Out

Create a “Homeowner’s Binder” to leave on the kitchen counter. Include appliance manuals, garage door openers, and a list of service contacts like your preferred HVAC technician or landscaper. This small gesture of goodwill goes a long way in ensuring a smooth transition. Finally, set up your mail forwarding through the USPS at least one week before you vacate. Ensure your closing is handled with professional precision by utilizing our Transaction Management services to oversee every step of this final transfer.

Closing Day: Signing the Deed and Cashing Out

The finish line is finally in sight. After weeks of managing inspections and disclosures, knowing what to do after accepting an offer on a house culminates in this single, decisive day. Your signing appointment is the moment legal ownership officially transfers to the buyer and your equity is converted into liquid capital. Bring your government-issued ID, all remaining keys, and your confirmed wiring instructions to the title company or attorney’s office. This appointment typically takes less than an hour, but it’s the most financially significant hour of the entire process.

Review your Closing Disclosure (CD) at least three days before this meeting. This document outlines every penny of the transaction. You’ll see the final sale price, prorated property taxes, and any HOA dues that were settled. Most importantly, you’ll see the massive disparity between your net proceeds and what you would’ve walked away with if you’d paid traditional realtor fees. In 2026, where seller closing costs already range from 1% to 3% of the sale price, protecting your equity from unnecessary commissions is the smartest financial move you can make.

As you finalize what to do after accepting an offer on a house, remember that the recording of the deed is the legal finish line. Once the county clerk records the transfer, the buyer’s lender releases the funds. This is when the transaction is officially “closed and funded.” You’ve successfully navigated the 2026 market by staying in the driver’s seat and prioritizing your own financial intelligence.

Understanding Your Net Proceeds

Verify that your settlement statement accurately reflects the flat-fee structure you chose. Ensure there are no hidden administrative fees or surprise brokerage charges. Confirm whether you want your funds delivered via a physical check or a direct wire transfer. If you choose a wire, the funds often hit your account on the same day the deed is recorded at the county office. This recording makes the sale a matter of public record and officially closes your chapter as the property owner.

The Congress Realty Advantage

Choosing the path of selling a house without a realtor doesn’t mean you’re alone. It means you’re in control. By using a Full Service Listing package, you’ve navigated the complexities of the 2026 market with professional tools while keeping your hard-earned equity where it belongs. You’ve mastered the roadmap and successfully protected your financial future. Ready to start your own success story? List your property on the MLS for a flat fee today and take command of your sale.

Take Command of Your Closing Today

You’ve navigated the complexities of the 2026 housing market and successfully reached the final stages of your sale. By mastering what to do after accepting an offer on a house, you ensure that every contingency is met and every deadline is honored without surrendering your equity to high commissions. Managing your own transaction is about more than just saving money; it’s about maintaining the confidence of being in total control of your financial future.

Since 2002, we’ve empowered sellers with the professional infrastructure needed to succeed. Whether you need professional CMA support to justify your price to an appraiser or expert Transaction Management to oversee the technical legal timeline, you have a reliable ally in your corner. You don’t need a traditional agent to achieve a professional result. It’s time to finalize your deal on your own terms and protect the equity you’ve built.

Your equity belongs in your pocket. Take the next step toward a smarter, more rewarding home sale and finish your transaction with the financial intelligence you deserve. You’ve got this.

Frequently Asked Questions

How long does it typically take to close after an offer is accepted?

Closing usually takes between 30 and 45 days. This timeline depends on the buyer’s loan type and the length of the contingency periods. Cash transactions move much faster, often reaching the finish line in 7 to 14 days. Understanding what to do after accepting an offer on a house involves tracking these milestones to ensure the lender meets the scheduled signing date.

Can a seller back out of an accepted offer on a house?

Backing out is difficult once the purchase agreement is signed. Sellers are legally bound to the contract unless the buyer fails to meet a deadline or a specific seller contingency isn’t met. If you attempt to cancel without a legal reason, the buyer could sue for “specific performance” to force the sale. Always review the default clauses in your agreement before making a move.

What happens if the buyer’s financing falls through at the last minute?

The contract typically terminates if the buyer has a financing contingency in place. In this scenario, the buyer usually receives their earnest money deposit back, and you must relist the property. To prevent this, confirm that the buyer has a strong pre-approval and monitor their loan progress throughout the escrow period. Keeping backup offers on file is a smart way to maintain your leverage.

Do I need a real estate attorney for the closing process?

Requirements vary by state. Some regions require an attorney to oversee the deed transfer and title review, while others rely entirely on escrow and title companies. Even if your state doesn’t mandate one, hiring an attorney can provide extra protection for complex transactions. Check your local regulations early so you can factor this into your closing timeline.

What is the difference between “Pending” and “Under Contract” on the MLS?

“Under Contract” means you’ve accepted an offer, but the buyer is still navigating contingencies like inspections or appraisals. “Pending” indicates that all contingencies have been cleared and the deal is simply waiting for the final signing. Knowing which status to use is a key part of what to do after accepting an offer on a house to manage buyer expectations.

Is the seller responsible for any costs on closing day?

Yes, sellers typically pay between 1% and 3% of the home’s sale price in closing costs. These expenses include title insurance, transfer taxes, and escrow fees. This is separate from agent commissions. By utilizing a flat-fee listing model, you eliminate the traditional 3% listing commission, which significantly increases the total net proceeds you’ll receive at the end of the day.

What should I do if the buyer asks for a price reduction after the appraisal?

You have three main options: reduce the price to match the appraisal, ask the buyer to cover the “appraisal gap” in cash, or meet in the middle. You can also challenge a low appraisal by providing a Comparative Market Analysis (CMA) with more recent sales data. If an agreement can’t be reached, the buyer may have the right to cancel and keep their deposit.

When do I officially get the money from the sale of my house?

You generally receive your funds on the day the deed is recorded at the county office or the following business day. The escrow agent will distribute the proceeds via wire transfer or a physical check once they confirm the legal transfer of ownership. Wire transfers are the fastest method, often appearing in your bank account just hours after the final documents are processed.

Did you know the national average real estate commission hit a five-year high of 5.70% in March 2026? It’s a massive expense that makes every dollar of your home equity more precious than ever. You likely feel the pressure to get your listing price exactly right, but determining fair market value for my home often feels like a guessing game. You worry that underpricing will leave money on the table, while overpricing might cause your listing to sit for 52 days or more. It’s a delicate balance, and you deserve to be in the driver’s seat.

It’s common to feel frustrated by the gap between an automated estimate and reality. This guide empowers you to take charge by mastering the professional methodology for pricing your property. You’ll learn how to protect your equity and ensure a swift sale by using data-backed strategies instead of outdated industry habits. We’ll show you how to use a Comparative Market Analysis (CMA) and professional industry databases to find your ideal price range. You will gain the confidence to defend your price during negotiations and maximize your returns by avoiding high-cost commission models.

Key Takeaways

Define Fair Market Value accurately to ensure you are targeting the specific number that dictates your final net proceeds.

Learn the professional methodology for determining fair market value for my home by filtering recent “Sold” data using the “Three S’s” framework.

Discover why automated algorithms often struggle with unique homes and how to verify the data behind the “Black Box.”

Use search bracket psychology to position your listing for maximum visibility among buyers using major online filters.

Access professional-grade data with a Comparative Market Analysis (CMA) to defend your price during negotiations while maintaining full control of your equity.

What Is Fair Market Value (FMV) in the 2026 Housing Market?

What is the actual price of your home? It isn’t the number on a tax bill or a speculative guess from an online algorithm. Understanding What Is Fair Market Value (FMV) is the first step toward a successful sale. Legally, FMV is the price that a willing buyer would pay a willing seller on the open market, provided neither is under pressure to act. In a cooling 2026 market where the median existing-home sales price is $417,800, getting this number right is the difference between a closed deal and a stale listing.

FMV is the only figure that truly dictates your final net proceeds. While you might have an emotional attachment to your property, the market remains objective. Today’s buyers are highly sensitive to interest rates, which sit at 6.56% for a 30-year fixed mortgage as of June 2026. This financial reality means buyers use strict digital search filters on the MLS. If your price is even slightly outside a major search bracket, like $450,000 versus $451,000, you could lose a significant portion of your potential audience. Determining fair market value for my home requires looking at these technical search habits just as much as the physical property itself.

With existing-home inventory at 4.4 months of supply, the market is more balanced than the frenzy of previous years. Homes are now sitting for a median of 52 days. This means you can’t afford to “test the market” with an inflated price. An accurate FMV ensures you capture attention in those critical first two weeks when buyer interest is at its peak. By focusing on data-backed values and professional fixed-fee listing models, you avoid the trap of price cuts that signal desperation to savvy buyers and their agents.

Market Value vs. Appraised Value

View an appraisal as the bank’s safety net. It’s a professional opinion of value required for a mortgage, but it doesn’t always reflect what a buyer is willing to bid. Market value is driven by emotion, competition, and current demand. If multiple buyers fall in love with your home, the market value might soar past the bank’s estimate. If that happens, you’ll need to know how to bridge the “appraisal gap” to protect your equity. Don’t let a conservative bank estimate dictate your ceiling when buyer demand suggests a higher price point.

Why Your Tax Assessment Is Not Your Sale Price

Your tax assessment is almost never an accurate reflection of what your home is worth today. Local governments use mass appraisal formulas that often lag behind the actual market by a year or more. Showing a buyer your tax assessment during negotiations can backfire. If the assessment is low, the buyer will use it as leverage to lowball you. If it’s high, it simply highlights a higher tax burden. When determining fair market value for my home, rely on recent “Sold” data from professional industry databases to justify your price rather than outdated government records.

How to Calculate Fair Market Value: A Step-by-Step Methodology

Pricing your home is a technical process, not an emotional one. To protect your equity, you must move beyond “gut feelings” and adopt a data-driven approach. When determining fair market value for my home, the goal is to replicate the logic a professional appraiser or a savvy buyer will use. Follow this structured five-step methodology to find your ideal listing price.

Step 1: Identify ‘Sold’ Comps. Look only at properties that have closed in the last 90 days. Active listings represent what sellers hope to get, but sold data represents what buyers are actually paying.

Step 2: Filter by ‘The Three S’s’. Narrow your list to homes with similar square footage (within 10-15%), style (don’t compare a ranch to a two-story colonial), and status.

Step 3: Perform Quantitative Adjustments. If a comparable home has a finished basement and yours doesn’t, you must subtract that value from their sale price to see how your home stacks up.

Step 4: Analyze ‘Days on Market’. With the national median at 52 days as of April 2026, look for homes that went pending in under 21 days. These “fast movers” indicate the price points currently triggering the most demand.

Step 5: Synthesize Your Range. Don’t settle on a single number. Create a strategic range that accounts for your home’s unique condition and current inventory levels.

This process aligns with official How to Calculate Fair Market Value protocols used by many state authorities. It ensures your price is defensible when a buyer’s agent tries to negotiate. If you want a professional head start, requesting a Comparative Market Analysis (CMA) can provide the verified data you need to skip the guesswork.

Selecting the Right Comparable Properties (Comps)

Ignore the “For Sale” signs in your neighborhood. Those prices haven’t been tested by a completed transaction yet. In the shifting 2026 market, where mortgage rates have recently fluctuated near 6.56%, the “90-day rule” is your best friend. Data older than three months likely reflects a different interest rate environment and won’t accurately predict today’s buyer behavior. Prioritize homes within your specific school district; even a half-mile difference can change the value if it crosses a district line.

Adjusting for Home Improvements and Deficiencies

Be honest about your home’s condition. While a new HVAC system adds peace of mind, it’s often considered an “invisible” upgrade that maintains value rather than spiking it. Conversely, a 10-year-old kitchen is no longer “new” in the eyes of a buyer. You must account for the depreciation factor. Assign specific dollar values to differences in lot size or curb appeal. If a comp has a professional landscape package and your yard is basic, adjust your target price downward to remain competitive. Determining fair market value for my home requires this level of objective scrutiny to ensure you don’t overprice and let the listing go stale.

The Limitations of Automated Valuation Models (AVMs)

Why do online estimates for the same house vary by tens of thousands of dollars? Most sellers start their journey by looking at a Zestimate or a Redfin Estimate, but these tools operate inside a “Black Box.” You cannot see the specific data points the algorithm chose or ignored. While some AVMs report high accuracy for cookie-cutter homes, that margin of error often widens to 15% or more for unique or rural properties. Determining fair market value for my home is a task that demands human intuition and verifiable data. Relying on an algorithm can lead to an unrealistic entry price and “listing fatigue.” With the median days on market reaching 52 days as of April 2026, an initial pricing error can derail your entire timeline. You need more than a guess to protect your equity.

The core problem with machine learning in real estate is its inability to prioritize context. An algorithm might see a home sale down the street and apply that price per square foot to your property without knowing your neighbor’s house was a complete fixer-upper. This lack of transparency forces you to trust a number you can’t explain. When you enter negotiations, “Zillow said so” is not a valid defense. You need a data-backed foundation that allows you to stand firm on your price with confidence.

Why Algorithms Miss Interior Condition

A computer cannot walk through your front door. It doesn’t know if you just installed premium hardwood floors or if the house needs a new roof. Algorithms miss the “feel” of a home, such as dated wallpaper or the quality of natural light. Determining fair market value for my home requires looking at these specific upgrades that a machine simply cannot quantify. While professional photography helps humans appreciate these details, a machine sees only pixels and metadata. Congress Realty uses CMAs to bridge this data gap, ensuring your price reflects the actual condition of your living space rather than just a zip code average.

AVMs and the ‘Herding’ Effect

AVMs are susceptible to the “herding” effect. If one neighbor sells their home at a massive discount due to a divorce or foreclosure, that single outlier can skew every automated estimate in your neighborhood for months. Sellers who trust these machines without verification often face forced price drops within the first 30 days of listing. To succeed, you need Strategic Pricing: Aligning FMV with Buyer Psychology. Always verify AVM data against actual MLS closing statements. This ensures your strategy is based on reality, not a mathematical glitch. Taking control of your data is the only way to safeguard your financial interests in a cooling market.

Strategic Pricing: Aligning FMV with Buyer Psychology

Pricing is more than just a calculation; it is a strategic marketing move. When you are determining fair market value for my home, you must think like a buyer browsing on a smartphone late at night. Most buyers use digital filters that move in $25,000 or $50,000 increments. If you price your home at $505,000, you are invisible to every buyer who capped their search at $500,000. By choosing $499,900 or even exactly $500,000, you capture two distinct search brackets. This strategy avoids the “no-man’s land” of pricing and keeps your listing active in the maximum number of search feeds.

The first 14 days of your listing are the most critical. This is when the “New Listing” alerts hit thousands of inboxes simultaneously. If you launch with an accurate FMV, you create a sense of urgency that motivates buyers to act. In a market where homes go to pending in around 21 days, a price that feels like a “deal” compared to local comps can trigger multiple offers. Conversely, pricing for a single, high-value buyer often leads to the 52-day median wait time or worse. Aim for a price that invites competition rather than one that tests a buyer’s patience. You want to lead the market, not chase it with price drops.

Understanding Search Algorithm Thresholds

Search engines on major platforms prioritize round numbers and specific thresholds. If you price at $501,000, you are effectively cutting your potential audience in half. Buyers rarely search for “up to $501k.” They search for “up to $500k.” Pricing just under or right on these thresholds ensures your home appears in the maximum number of saved searches. This psychological perception is what drives high click-through rates and more showings in your first week. It’s a simple adjustment that yields massive visibility.

The Danger of Emotional Pricing

Your home is a collection of memories, but to a buyer, it is a financial asset. Avoid the trap of pricing based on what you need to net for your next down payment or what you spent on that custom patio years ago. The market does not care about your labor costs; it only cares about current utility and demand. To remain objective, use a Comparative Market Analysis to ground your decisions in hard data. Separating your emotions from the transaction is the only way to protect your equity. Ready to see the data for yourself? Get your professional CMA today and start your listing with confidence.

Securing Your Value: The Professional CMA Advantage

Why should you rely on a professional Comparative Market Analysis (CMA) instead of a simple online estimate? A CMA is the gold standard for independent sellers because it uses the same verified industry databases that traditional agents use. When you are determining fair market value for my home, a CMA provides the technical justification for your price. It isn’t just a suggested number; it’s a comprehensive report that compares your property to recent sales with granular accuracy. This level of detail is essential for defending your equity during negotiations. If a buyer’s agent tries to lowball your offer, you can present the data-backed findings of your CMA to stand your ground.

A professional CMA protects your interests by:

Providing data-backed evidence to justify your price to skeptical buyers.

Identifying the most relevant local comps that algorithms often miss.

Allowing you to adjust for specific home improvements with dollar-for-dollar accuracy.

Accurate pricing is the single most effective way to protect your home equity. In a market where the median days on market is 52, you can’t afford to waste time with an incorrect price. Overpricing leads to stale listings, while underpricing leaves money on the table. Congress Realty provides the professional infrastructure of a traditional broker without the traditional 3% listing commission. This pragmatic approach allows you to retain the maximum amount of your equity while still benefiting from professional-grade transaction management. You maintain full command over the process, using the same tools as the pros to ensure a swift and profitable sale.

The Congress Realty Approach to Valuation

Our Standard and Full Service packages are designed to provide the specific valuation support you need to win. You’ll benefit from having a broker-owner oversee your transaction management, ensuring that every legal and logistical detail is handled correctly. This professional oversight gives you the confidence to manage the sale independently. Remember that listing on the MLS without a realtor requires professional-grade pricing to capture the attention of buyers and their agents. Determining fair market value for my home with our expert tools ensures your listing is competitive from the very first day.

Next Steps: From Valuation to Listing

Once you have synthesized your data into a strategic price range, you can transition to a live MLS listing in as little as 24 hours. Use this time to prepare your home to meet the FMV you’ve established. Professional photography, deep cleaning, and minor staging can help your property match the high-value comps in your CMA. When your home looks its best and is priced accurately, the market will respond. Take control of your financial future and stop paying for services you can manage yourself. Start your equity-first listing with Congress Realty today and experience a smarter way to sell.

Take Command of Your Home Equity Today

You now have the professional methodology needed to price your property with absolute precision. By focusing on recent sold data and understanding search algorithm thresholds, you can avoid the common pitfalls of overpricing or relying on flawed automated estimates. Determining fair market value for my home is no longer a guessing game; it’s a strategic advantage that puts you in control of your financial outcome. You don’t need a high-cost agent to tell you what your house is worth when you have access to the right data.

Congress Realty has provided broker-led transaction management since 2002. Our model is built specifically to empower independent sellers like you. Every listing package we offer includes a professional Comparative Market Analysis (CMA) to ensure your price is backed by the same industry databases the pros use. This allows you to save the traditional 3% listing commission while maintaining the professional infrastructure required for a successful sale. Stop leaving your equity to chance and start making informed, intelligent decisions.

How do I determine the fair market value of my home for free?

You can find a baseline by researching “Sold” listings on public real estate websites. Focus on properties within a half mile radius that closed within the last 90 days. While these free tools provide a ballpark figure, they often lack the depth of professional databases. For a more precise number, many sellers find that a professional Comparative Market Analysis (CMA) offers the accuracy needed to protect their equity.

Is fair market value the same as the Zestimate?

A Zestimate is a starting point, but it is not a legal or financial substitute for fair market value. Algorithms use public data that may not reflect recent interior upgrades or specific neighborhood nuances. Zillow reports a median accuracy of 2.4% for on-market homes, yet this margin can widen significantly for unique properties. Determining fair market value for my home requires a human touch to verify the data behind the machine’s guess.

Can I use an appraisal from two years ago to price my home today?

Avoid using old appraisals because the 2026 market is vastly different than it was two years ago. Mortgage rates for a 30-year fixed loan sit at 6.56% as of June 2026, which has significantly changed buyer purchasing power. Since median home prices have declined for five consecutive quarters, relying on outdated valuations will almost certainly lead to overpricing. You need fresh data from the last three months to stay competitive.

What happens if I price my home above fair market value?

Overpricing your home usually results in your listing sitting on the market for much longer than the national median of 52 days. When a house lingers, buyers assume something is wrong with the property, which often leads to lowball offers. You’ll likely end up chasing the market with price drops. It’s much more effective to launch with a data-backed price that triggers immediate interest and potential multiple offers.

How often does fair market value change in a hot market?

Fair market value can shift every few weeks depending on inventory levels and mortgage rate volatility. In May 2026, rates jumped to a nine-month high of 6.65% before stabilizing. These micro-shifts directly impact what buyers can afford to bid. If you’re in a high-demand area, check local “Pending” and “Sold” statuses every two weeks to ensure your listing price still aligns with the current reality.

Does a professional CMA guarantee my house will sell at that price?

A professional CMA provides a data-backed price range, but it is not a guaranteed sale price. It acts as a strategic map based on what other buyers have recently paid for similar homes. The final number depends on your home’s condition, your staging, and how well you negotiate. Think of the CMA as your defensive shield; it gives you the evidence needed to justify your asking price to skeptical buyers.

Should I include the cost of my recent renovations in the FMV?

Focus on the market’s perceived value of your upgrades rather than the actual amount you spent on labor and materials. Buyers don’t pay dollar-for-dollar for your costs; they pay for the finished result. For example, a minor kitchen refresh might offer a higher return on investment than a luxury pool in a mid-range neighborhood. Use your CMA to see how much “value-add” similar renovated homes actually commanded in recent sales.

How do I find ‘sold’ comps if I’m not a real estate agent?

You can access “Sold” data through public records or by using professional listing services that provide MLS-integrated reports. Determining fair market value for my home is much simpler when you use the same professional infrastructure as traditional brokerages. By looking at actual closing statements rather than just “Active” asking prices, you gain a clear, unfiltered view of what the market is truly willing to pay in 2026.

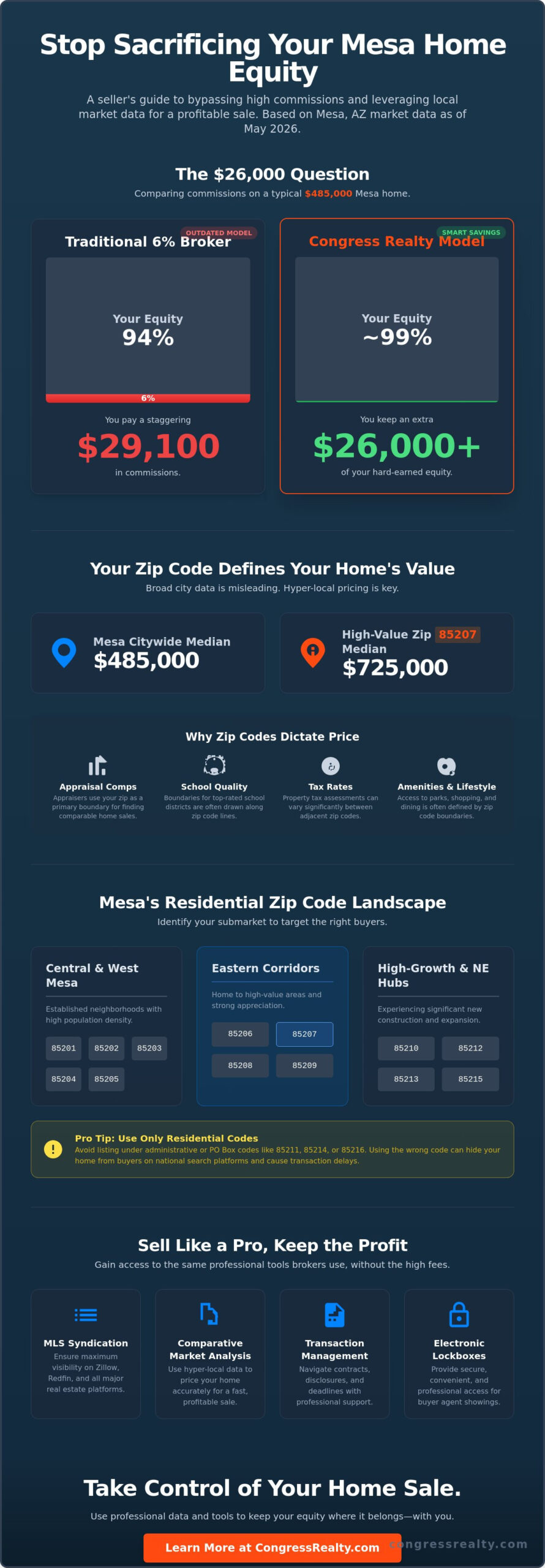

Why sacrifice over $26,000 in equity just because a traditional broker insists on a 6% commission? With Mesa’s median home price at $485,000 as of May 2026, those legacy percentages represent a significant financial loss that savvy sellers no longer need to accept. You know your neighborhood better than anyone, yet the lack of transparent market data often makes the selling process feel like a mystery. It’s frustrating to watch your hard-earned profit disappear into someone else’s pocket through outdated fee structures.

This guide provides a definitive list of mesa az zip codes and reveals how to use geographic insights to list your home professionally while bypassing high commissions. We’ll show you how to take command of your sale by utilizing the same tools the pros use, such as a Comparative Market Analysis and professional transaction management. You’ll discover how to navigate diverse submarkets, from the high-value 85207 area to the growth hubs in the southeast, ensuring you lead the process with total confidence and keep your equity where it belongs.

Key Takeaways

Access the definitive 2026 list of residential mesa az zip codes to pinpoint your property’s specific submarket and buyer demographic.

Learn how to decode the “Zip Code Premium” and use a professional Comparative Market Analysis to price your home for a fast, profitable sale.

Understand how the MLS uses geographic data to syndicate your listing to national platforms, ensuring maximum visibility without traditional high-cost brokers.

Calculate your potential equity savings by comparing legacy 6% commissions against a modern, fixed-cost listing model that puts you in control.

Identify the essential professional tools, including electronic lockboxes and transaction management, that simplify the process of selling your home independently.

Precision is the first step toward a successful sale. Mesa covers 138 square miles of the East Valley, making it a sprawling urban center where geographic boundaries define property values and buyer interest. As the third-largest city in Mesa, Arizona, this region has seen its residential lines shift alongside rapid population growth. You must identify your exact five-digit code before entering any legal documentation or professional listing database. Using the wrong mesa az zip codes can cause your property to be suppressed on national search platforms, effectively hiding your home from qualified buyers.

It’s vital to distinguish between residential zones and administrative codes. While Mesa utilizes several codes, only 13 are designated for primary residential use. Codes such as 85211, 85214, 85216, 85274, 85275, and 85277 are typically reserved for PO boxes or specific commercial entities. If you mistakenly list your home under one of these administrative codes, you’ll likely face technical errors during the transaction management phase. Stick to the residential list below to ensure your listing propagates correctly across the MLS and third-party sites.

Primary Residential Zip Codes

The city’s residential landscape is divided into distinct corridors, each with its own market temperature and inventory levels. Use this breakdown to verify your location:

Central and West Mesa: 85201, 85202, 85203, 85204, and 85205. These areas feature established neighborhoods and high population density.

Eastern Corridors: 85206, 85207, 85208, and 85209. This includes the high-value 85207 area, which saw median prices reach $725,000 as of May 2026.

High-Growth and Northeast Hubs: 85210, 85212, 85213, and 85215. These zones are currently experiencing significant new construction and expansion.

Why Geographic Accuracy Matters in 2026

In a balanced market where the average home stays on the market for 65 days, you can’t afford technical delays. Search algorithms on major real estate sites rely heavily on zip code filters. If your code is inaccurate, your home won’t appear when a buyer searches for their preferred school district or neighborhood. Accuracy also dictates your tax assessment and the Comparative Market Analysis (CMA) used to justify your asking price. Professional listing services require this data to be perfect. By confirming your mesa az zip codes early, you protect your autonomy and ensure your listing remains visible to the thousands of agents searching the professional databases every day.

Valuation Dynamics: How Zip Codes Impact Home Prices

Does a single digit in your address really change what your home is worth? In short: absolutely. Real estate appraisers and sophisticated buyers view mesa az zip codes as more than just mail delivery routes; they’re shorthand for school quality, property tax rates, and lifestyle amenities. Understanding how your address affects home value is critical for any seller who wants to avoid leaving money on the table. For instance, while the citywide median price was $485,000 in May 2026, homes in the 85207 corridor commanded a median of $725,000. This massive spread demonstrates why you can’t rely on broad city data to price your specific property.

Appraisers use your zip code as the primary boundary for their search. They look for “bracketed” comps, which means they search for sold properties similar in age and size within the same geographic code. If they have to cross into a different zip code to find a match, they often apply location adjustments that can lower your appraisal value. Historical trends also show that some Mesa codes appreciate faster than others. For example, the southeast growth hub near Cadence at Gateway has seen more aggressive price stability than central areas with older housing stock. A single street can represent a shift of tens of thousands of dollars if it crosses a zip code boundary.

Comparative Market Analysis (CMA) by Zip Code

To capture this “Zip Code Premium” accurately, you need a professional Comparative Market Analysis. A CMA filters out irrelevant data from neighboring districts and focuses strictly on homes that share your geographic advantages. If you price your home based on Mesa’s 98% sale-to-list ratio without looking at your specific street, you might underprice a high-demand area or overprice an older submarket. Micro-markets can shift significantly across a single major intersection. By looking at hyper-local comps, you ensure your listing is competitive from day one.

Market Trends and Buyer Behavior

Buyer behavior in 2026 is data-driven. Many buyers set their search alerts for specific mesa az zip codes to stay within certain school boundaries or close to major employers like Boeing. When demand spikes in a specific code, it triggers bidding wars that aren’t reflected in the broader city stats. Currently, the market is balanced with an average of 65 days on market, but some southeast zip codes move much faster due to new construction in Eastmark. Watching these trends allows you to time your listing for maximum exposure. If you’re ready to see how your neighborhood stacks up, reviewing a professional market report is a smart way to maximize your equity.

The Role of Zip Codes in Multiple Listing Services (MLS)

How do thousands of active buyers find your home in a city of 517,500 people? The answer lies in the Multiple Listing Service (MLS), the professional database where every licensed agent starts their search. In this digital ecosystem, mesa az zip codes serve as the primary routing instructions. If your zip code data is inaccurate, your home effectively vanishes from the filtered searches that matter most. It doesn’t matter how beautiful your professional photography is if the technical data blocks the listing from appearing in a buyer’s inbox. Accuracy is the technical bridge between your front door and a buyer’s screen.

When you list your property, you’re competing for attention in a market with approximately 138 square miles of inventory. The MLS acts as the central nervous system for these transactions. It uses geographic markers to syndicate your property data across a massive web of national sites like Zillow and Realtor.com. According to the U.S. Census Bureau Mesa Data, the city contains over 210,000 housing units. Without precise tagging of your specific location, your home would be lost in a sea of data. Securing your spot on the professional list of multiple listing services ensures that your home isn’t just for sale; it’s visible to every brokerage in the state.

Syndication and Search Algorithms

Modern buyers don’t browse; they filter. They set up Save Search alerts based on specific geographic boundaries. When your property is uploaded with the correct mesa az zip codes, the MLS triggers an immediate notification to every buyer whose criteria match your neighborhood. This automated syndication is what drives the 65-day average on market. If your geographic tagging is off by even one digit, you miss the critical first 48 hours of listing momentum when buyer interest is at its peak.

Visibility Without the 3% Commission

You don’t need to pay a traditional 3% listing commission to gain this level of professional exposure. The disruptive flat-fee model provides you with the exact same MLS infrastructure used by high-cost brokerages. You maintain total control over your property data while appearing in the same professional databases as every other listing. By utilizing tools like an electronic lockbox and professional transaction management, you lead the process with the same authority as a legacy agent. You get the visibility you need while keeping your equity where it belongs: in your pocket.

Leveraging Zip Code Data for a Successful Independent Sale

Data is the ultimate equalizer in real estate. You don’t need a traditional broker to interpret market conditions when you have access to the same geographic metrics they use. By mastering the specifics of mesa az zip codes, you transition from a passive seller to an informed market lead. Taking command of your sale starts with understanding that your “neighborhood” isn’t just the houses on your block; it’s a data-driven micro-market defined by five digits. Use this information to build a strategy that protects your equity and attracts the most qualified buyers in the East Valley.

DIY Market Research for Sellers

Start your research by filtering recent sales data strictly within your zip code. While Mesa’s citywide median home price sits at $485,000, your specific area might be trending higher or lower based on recent activity. Look for “Sold” listings from the last 90 days to find your true competition. Pay close attention to the “Days on Market” metric. If the Mesa average is 65 days but homes in your specific code are selling in 40, you have a high-demand listing that justifies a firmer asking price. Identifying this “sweet spot” ensures you don’t leave money on the table or scare away buyers with an unrealistic figure. You can use a professional Comparative Market Analysis to verify these findings and gain the same level of insight as a high-commission agent.

Strategic Marketing for Your Neighborhood

Your marketing should speak directly to the lifestyle your specific zip code offers. If you’re listing in 85212 or 85213, highlight the proximity to high-growth hubs like Eastmark or the master-planned amenities that drive buyer interest in the southeast. For those in 85215, emphasize the connection to major employers like Boeing. Use this geographic context in your listing description to trigger keywords that buyers actually search for. Stand out from the competition by investing in professional photography; in a digital-first market, your first showing happens on a smartphone screen. Combine these visuals with a professional yard sign and an electronic lockbox to make the showing process seamless for local buyers. This level of professional infrastructure signals to everyone involved that you’re a savvy seller in total control of the transaction.

Ready to turn your market research into a professional listing? List your home on the MLS today and keep thousands more of your equity by choosing a modern, fixed-cost model.

Saving Your Equity: Flat Fee MLS Solutions Across All Zip Codes

Why pay a legacy broker a massive percentage of your home’s value when the heavy lifting of market research is already done? Whether your property is nestled in the luxury pockets of 85207 or the high-growth corridors of 85212, the logic remains the same: you shouldn’t pay for a brand name when you can buy the results. Our flat-fee model works across all mesa az zip codes to ensure that your equity stays in your bank account rather than being split among traditional agents. You’ve mastered the geographic data; now it’s time to claim the financial reward.

The numbers in 2026 tell a clear story. With Mesa’s median home price at $485,000, a traditional 6% commission would strip over $29,000 from your closing proceeds. By choosing a modern listing solution, you can easily save $15,000 or more on a standard home sale. Learning how to sell a house without a realtor is the single most impactful financial decision you can make as a homeowner this year. This approach also allows you to position your home as a “smart buy.” You can choose to pass a portion of those savings to the buyer to trigger a faster sale or keep the entire surplus as your own profit.

The Congress Realty Advantage

We provide the professional infrastructure you need to compete with high-commission listings without the high-commission price tag. Our services cover every residential pocket within the mesa az zip codes, offering you parity with the biggest brokerages in the state. When you list with us, you receive a professional Comparative Market Analysis to nail your pricing, an electronic lockbox for secure showings, and full transaction management to handle the paperwork. You become the designated broker of your own equity, supported by the same professional databases that every licensed agent uses.

Getting Started with Your Listing

Transitioning from researching data to closing your sale is a straightforward process. First, select the listing package that aligns with your specific timeline and service needs. You’ll then submit your property details and professional photography through our streamlined platform. We ensure your data is perfectly formatted for the MLS, triggering those all-important search alerts for active buyers. Within days, your home will be visible on every major national real estate site. You take the lead on showings and negotiations, while we provide the professional backbone to ensure a smooth, legally sound closing. Take control of your financial future today and start your listing with the confidence of a market expert.

Take Command of Your Mesa Home Sale

Mastering the nuances of mesa az zip codes is the first step toward a high-equity closing. You now have the geographic data and strategic insights needed to navigate Mesa’s balanced market with total confidence. By focusing on hyper-local comps and ensuring technical accuracy on the MLS, you position your property for maximum visibility without the burden of a traditional listing commission.

It’s time to put these tools to work. Since 2002, Congress Realty has empowered thousands of homeowners to finalize successful closings while maintaining an A+ rating with the Better Business Bureau. You don’t need a high-cost broker to lead your transaction; you simply need the right professional infrastructure. Our model allows you to save an average of 3% on every transaction, keeping your hard-earned equity exactly where it belongs.

There are 13 primary residential zip codes in Mesa used for real estate listings. These include 85201, 85202, 85203, 85204, 85205, 85206, 85207, 85208, 85209, 85210, 85212, 85213, and 85215. While other codes like 85211 or 85274 exist for administrative purposes and PO boxes, they aren’t used for residential property addresses. Understanding these specific mesa az zip codes ensures your property is categorized correctly within professional databases.

What is the most expensive zip code in Mesa for 2026?

The 85207 zip code remains the most expensive area in Mesa as of May 2026. With a median sale price of $725,000, this northeast corridor commands a significant premium compared to the citywide median of $485,000. This region is highly sought after for its luxury master planned communities and scenic desert views, making it a high demand zone for buyers looking for premium inventory in the East Valley.

Do I need a local agent to list my home on the MLS in a specific zip code?

No, you don’t need a traditional local agent to gain professional MLS exposure in any neighborhood. Modern flat fee listing services provide the exact same technical infrastructure and syndication to national sites like Zillow and Realtor.com. By using a professional listing service, you maintain total control over your transaction and keep more of your equity while appearing in the same database as high commission listings in your area.

How do zip codes affect my home’s property taxes?

Zip codes often serve as the primary boundaries for various taxing authorities and school districts. Your specific address determines which municipal bonds, school levies, and special assessment districts apply to your property. Since tax rates can vary between different mesa az zip codes, buyers often filter their searches based on these carrying costs. Accurate geographic data ensures that your property’s total cost of ownership is represented correctly to potential buyers.

Can I change the zip code on my real estate listing if it is near a border?