What if that “insulting” lowball offer sitting in your inbox is actually the key to your most successful closing yet? It’s easy to feel disrespected when a buyer ignores your $420,000 asking price and submits a bid that feels like a joke. However, learning how to handle lowball offers fsbo isn’t about defending your pride; it’s about mastering a data-driven opening move. With active housing inventory up 1.8% year-over-year, buyers are testing the waters, but you hold a significant 3% commission advantage that traditional sellers simply don’t have.

We understand the anxiety of feeling bullied by buyers who think they can take advantage of a private seller. This article will show you exactly how to flip the script and maintain total control of your sale. You’ll gain a concrete counter-offer script, a professional method to determine if the market has truly shifted, and strategies to turn a low bid into a signed contract. It’s time to protect your equity and prove that managing your own sale is both simple and highly rewarding.

Key Takeaways

Identify why buyers target independent sellers and learn how to debunk the myth that your commission savings belong to the buyer.

Discover how a professional Comparative Market Analysis (CMA) provides the data-driven authority needed to silence lowball justifications.

Master three specific strategies on how to handle lowball offers fsbo, including the “Equity-First” counter-offer that protects your bottom line.

Learn to negotiate high-value terms like shortened inspection periods or cash closing advantages to strengthen a deal without dropping your price.

Understand how professional photography and maximum MLS exposure create the competitive environment necessary to spark bidding wars.

Understanding the Lowball Offer: Why Buyers Test FSBO Sellers

Entering the market as a For Sale By Owner (FSBO) seller is an empowering choice, but it often makes you a target for specific buyer tactics. These buyers aren’t necessarily looking for a home; they’re looking for a deal at your expense. In a professional real estate context, a lowball offer is typically defined as any bid sitting 10% to 25% below the fair market value. With national median home prices hovering between $417,800 and $429,300 in 2026, a 20% lowball could mean a staggering $85,000 hit to your equity. Knowing how to handle lowball offers fsbo starts with recognizing that these numbers aren’t personal insults. They’re tactical maneuvers designed to see if you know your home’s true worth.

Many buyers walk into a private sale assuming they’re entitled to what we call the “FSBO Discount.” They see the 3% commission you’re saving by not using a traditional listing agent and immediately subtract it from their offer. This is a logical fallacy. You aren’t saving that 3% to give it to the buyer; you’re saving it to keep it in your pocket. Don’t let a buyer convince you that your financial intelligence should result in a lower sales price. With active housing inventory up 1.8% year-over-year, buyers have more choices, but that doesn’t mean your equity is up for grabs.

The Psychology of the “Fishing” Offer

Professional investors and house flippers often swarm new listings within the first 48 hours. They’re “fishing” for sellers who might be anxious about the process or unsure of their pricing. A serious buyer with a low budget will often lead with praise for the home and a request for help. A predatory offer, however, is usually cold, aggressive, and filled with “take it or leave it” language. The Anchor Effect is a cognitive bias where a buyer presents an initial low number to psychologically tether your expectations and make their subsequent, slightly higher offers seem more reasonable.

Why Your Response Sets the Tone for the Whole Deal

It’s tempting to tell a lowballer to “pound sand” or simply ignore the email. Resist that urge. Silence can kill a potential sale before it even starts. Learning how to handle lowball offers fsbo with a professional, data-backed reply signals that you are not a desperate seller. By responding with logic rather than emotion, you transform from a target into a formidable negotiator. You have the data, you have the equity, and you have the control. A pragmatic response proves that you aren’t desperate; you’re just waiting for the right partner for a successful closing.

Removing Emotion: Using a Comparative Market Analysis (CMA) to Pivot

When you receive an offer that feels like a gut punch, your first instinct might be to take it personally. You think about the upgrades you’ve made, the memories in the home, or the specific dollar amount you need to fund your next move. However, your personal financial “need” is irrelevant to a buyer. To win this negotiation, you must shift the conversation from feelings to facts. This is where a professional Comparative Market Analysis (CMA) becomes your most powerful tool. By grounding your response in real estate negotiation principles, you move the goalposts from “What I want” to “What the market demands.”

A professional CMA silences lowball justifications by providing a cold, hard look at the competition. It’s not just a list of homes; it’s a strategic map. If a buyer claims your price is too high, you don’t argue. You simply attach the CMA to your counter-offer. This objective proof forces the buyer to either dispute the data or admit they’re fishing for a discount. If you’re wondering how to sell your house on your own while maintaining a firm price point, the answer lies in the quality of your data. Using how to handle lowball offers fsbo strategies effectively means letting the numbers do the heavy lifting for you.

Analyzing Recent Comparable Sales (Comps)

Success depends on the freshness of your data. In the 2026 market, where active inventory has increased by 1.8%, a comp from six months ago is “stale” and useless. Focus exclusively on homes sold within a 1-mile radius in the last 90 days. You must also adjust for features that buyers often overlook. If your home features Professional Photography or high-end kitchen upgrades that the “sold” comps lacked, these are value-drivers that justify your higher asking price. If you haven’t yet secured a professional market analysis, now is the time to arm yourself with one.

The “Market Reality” Comparison

Buyers often use vague market sentiment to justify low bids. Use this comparison table to pivot back to reality:

Buyer Claim

CMA Fact

“The market is cooling down significantly.”

Average Days on Market (DOM) in this zip code is currently 14 days.

“Your home is priced above the neighborhood average.”

Three identical models within 0.5 miles sold for $425,000 last month.

“Inventory is too high; I have plenty of options.”

Only two other homes with your specific square footage are active.

Professional CMA data is the only language a lowballer respects because it transforms a subjective argument into an objective financial reality. When you respond with a table like this, you aren’t just a seller; you’re a market expert in total command of the transaction.

3 Strategic Ways to Respond to Lowball Offers

Speed is your greatest ally when a low bid hits your inbox. A buyer who sends a lowball offer is often testing your resolve to see how quickly you’ll fold. Respond within 24 hours to maintain momentum and signal that you are a professional, active participant in the sale. Delaying your reply out of frustration only gives the buyer time to find another property. By staying engaged, you keep the door open for a successful closing while proving you are in total command of the process. Here are three proven strategies for how to handle lowball offers fsbo without sacrificing your equity.

The Equity Advantage Counter-Offer

As a private seller, you possess a powerful negotiation tool that traditional sellers lack: the 3% commission buffer. Most sellers are prepared to lose 5% to 6% of their sale price to agent fees. Because you’ve chosen a smarter path, you can use a portion of those savings to find a middle ground that feels like a win for the buyer while still netting you more than a traditional sale. Start by understanding realtor commissions and how they impact a standard net sheet. If a buyer asks for a $15,000 discount, you might offer a $5,000 credit. You’re still saving $10,000 compared to a legacy brokerage model, and the buyer feels they’ve won a concession. It’s a pragmatic, benefit-driven approach that protects your bottom line.

The Professional Script for a Hard Reject

Sometimes an offer is so low that it doesn’t warrant a numerical counter. In these cases, use a “Hard Reject” with a polite invitation to try again. This signals that you aren’t desperate and won’t be bullied. Use this specific script: “We appreciate your interest in the property. However, based on recent comparable sales, we are only entertaining offers within 2% of our asking price at this time. If you’d like to submit a revised offer, we would be happy to review it.” This shuts down “bottom-feeder” tactics immediately. It identifies the time-waster buyer who is just fishing for a steal and frees you up to focus on serious prospects. You are providing a “full service” experience through your professionalism without paying the high-cost industry fees.

The Data-Backed Pivot

If your CMA confirms your price is spot-on, don’t budge. Counter at your full asking price and include the data as an attachment. This is the ultimate power move in how to handle lowball offers fsbo. You aren’t being stubborn; you’re being factual. Tell the buyer: “Our price is based on the three most recent sales within a mile of this home, which averaged $425,000. We have attached the report for your review.” This forces the buyer to argue with the market rather than with you. It’s a direct, action-oriented way to maintain your price point while showing the buyer exactly why your home is worth every penny.

Negotiating Terms Beyond the Sale Price

Price is only one component of a real estate contract. When you’re figuring out how to handle lowball offers fsbo, it’s vital to remember that a “clean” offer is often superior to a high-priced one riddled with complex contingencies. A cash offer at $415,000 is frequently more valuable than a financed offer at $425,000. Why? Because cash eliminates the risk of a low appraisal or a mortgage falling through at the eleventh hour. With 30-year fixed mortgage rates currently between 6.51% and 6.68%, financing is a significant variable in 2026. Removing that hurdle provides a level of certainty that is worth its weight in gold.

You can also trade a price concession for an “As-Is” agreement. This allows you to walk away without the obligation of fixing a leaky faucet or replacing an aging HVAC system. If you need more time to transition, negotiate a post-closing occupancy agreement. This “lease-back” gives you the freedom to move on your own schedule, potentially saving you thousands in temporary housing or storage fees. These pragmatic adjustments keep you in control of your financial outcome while simplifying the entire process.

Closing Dates and Contingencies

Momentum is essential for a secure transaction. Shorten the inspection period from the standard ten days to five. This forces the buyer to move quickly or move on. Most importantly, refuse any “home sale contingency” that makes your closing dependent on the buyer selling their current property. This is a common trap that can leave your home sitting in “pending” status for months. Utilizing Transaction Management services ensures these specific terms are legally sound and tracked with professional precision, giving you the confidence of an expert without the traditional 3% listing commission.

Earnest Money and Buyer Skin in the Game

If a buyer submits a low offer, demand they put more “skin in the game.” Request an earnest money deposit of 1% to 2% of the sale price rather than a small flat fee. Structure the agreement so this deposit becomes non-refundable once the inspection period ends. This filters out non-serious “bottom-feeders” immediately. Beyond the contract, use an Electronic Lockbox to monitor activity. This technology provides a digital trail of every professional who enters your home, allowing you to gauge real interest levels before an offer even hits your inbox. Mastering these variables is the smartest way to protect your equity while maintaining total command of the sale.

Leveraging Professional MLS Tools to Secure Higher Offers

The best way to manage a low bid is to prevent it from ever reaching your inbox. Most “bottom-feeder” buyers target private listings because they detect a lack of professional infrastructure. When your home is presented with Professional Photography, it eliminates the “perceived flaw” discount that buyers often apply to amateur-looking listings. High-quality visuals signal that the property is well-maintained and highly valued, forcing buyers to start their offers at a more respectful level. By investing in the right presentation, you’ve already won half the battle in how to handle lowball offers fsbo.

Beyond aesthetics, the use of an Electronic Lockbox serves as a critical security and screening tool. This technology ensures that only qualified buyers accompanied by licensed agents can enter your home. It creates a digital trail of every showing, providing you with real-time data on market interest. This professional transparency tells buyers and their agents that you are a savvy, independent seller who understands the mechanics of a modern real estate transaction. You aren’t just selling a house; you’re managing a professional business deal.

Exposure as Your Best Defense

Scarcity drives value. If only one person knows your home is for sale, they have all the leverage. If thousands know, the power shifts back to you. Securing a flat fee mls listing is the single most effective way to attract serious, high-intent buyers. The Multiple Listing Service (MLS) is the ultimate filter for “bottom-feeders” because it forces every inquiry to pass through the professional infrastructure of a registered agent. This exposure creates the “MLS Effect,” where the threat of a competing offer keeps buyers from submitting lowball bids. Once you accept a fair offer, you can utilize “Full Service” support to manage the complex paperwork and ensure the deal stays on track toward a successful closing.

The Congress Realty Advantage

Choosing between a Standard Listing and a Full Service Listing allows you to tailor the level of support to your specific comfort level. Both options provide the professional parity needed to command top dollar in the 2026 market. One of the greatest risks after accepting an offer is “price chipping,” where a buyer tries to renegotiate the price downward during the inspection period. Our Transaction Management services provide the professional oversight necessary to prevent these tactics, keeping the buyer accountable to the original contract terms. You have the command, and we provide the infrastructure. List your home professionally today and keep your equity.

Take Command of Your Equity Today

Mastering how to handle lowball offers fsbo is the final step in shifting from a defensive seller to a savvy market negotiator. You’ve learned that a low bid isn’t a personal insult; it’s a tactical opening move that you can dominate with the right data. By using a professional CMA to anchor your price and negotiating terms like cash closings or “as-is” agreements, you protect your hard-earned equity from predatory tactics. You hold the 3% commission advantage, and it’s time to use it.

Since 2002, Congress Realty has provided the national professional oversight and infrastructure needed to disrupt the high-cost brokerage model. You don’t need a 6% commission to get expert results. With tools like professional photography, electronic lockboxes, and dedicated transaction management support, you stay in total control of your closing from start to finish. Save your equity and list on the MLS for a flat fee today. You have the financial intelligence to manage your own sale, and we provide the professional tools to make it simple and rewarding.

Frequently Asked Questions

Is a lowball offer better than no offer at all?

A lowball offer is often better than no offer because it proves your listing is attracting active interest in the 2026 market. It provides an immediate opportunity to engage a buyer and test their true motivation. Even a bid 20% below asking can be negotiated upward once you present objective market data and prove you aren’t a desperate seller.

Should I even bother countering an offer that is 20% below asking?

You should always bother countering unless the buyer refuses to provide a pre-approval letter or proof of funds. Many serious buyers start low to see how much “equity room” you have. Countering with a firm number backed by a professional CMA signals that you are an expert who knows the home’s true value and won’t be bullied.

How do I tell a buyer their offer is too low without sounding rude?

Focus on the data rather than your personal feelings to keep the transaction professional and pragmatic. Use a script like, “We appreciate your interest, but based on recent comparable sales in this zip code, we cannot accept an offer at this level.” This keeps the door open for a higher bid while maintaining your position of strength.

Why do buyers lowball FSBO sellers more than traditional listings?

Buyers often assume private sellers are less informed about current market trends or are in a hurry to sell. They try to capture your 3% commission savings for themselves. Learning how to handle lowball offers fsbo involves proving these assumptions wrong by using professional tools like electronic lockboxes and transaction management to show you have a professional infrastructure in place.

Can I ignore a lowball offer if I am selling my own home?

You have the right to ignore any offer, but a strategic seller uses every inquiry as a chance to close. Ignoring an offer can kill momentum and discourage a buyer who might have been willing to pay more after a reality check. A short, professional rejection or a data-backed counter-offer is a more effective way to maintain control of the sale.

What is the “Equity Advantage” when negotiating a FSBO sale?

The Equity Advantage is the roughly 3% of the sale price you save by not paying a traditional listing commission. This buffer gives you more room to negotiate than a seller paying a 6% total fee. You can offer small credits or concessions to the buyer while still netting significantly more money than you would with a legacy brokerage model.

How does a professional CMA help in a lowball negotiation?

A professional CMA provides the objective evidence needed to shut down lowball justifications immediately. When a buyer claims the market is slow, you can point to the average 14 days on market for similar homes in your neighborhood. It shifts the negotiation from an emotional argument to a factual discussion about current neighborhood prices that the buyer cannot easily ignore.

What should I do if a buyer refuses to come up from their lowball price?

If a buyer refuses to move toward a fair market price, you should walk away and focus on new leads. Your how to handle lowball offers fsbo strategy depends on finding a serious partner, not a “bottom-feeder” investor looking for a steal. Maximum MLS exposure ensures that a more reasonable buyer will eventually see the value in your property and offer a fair price.

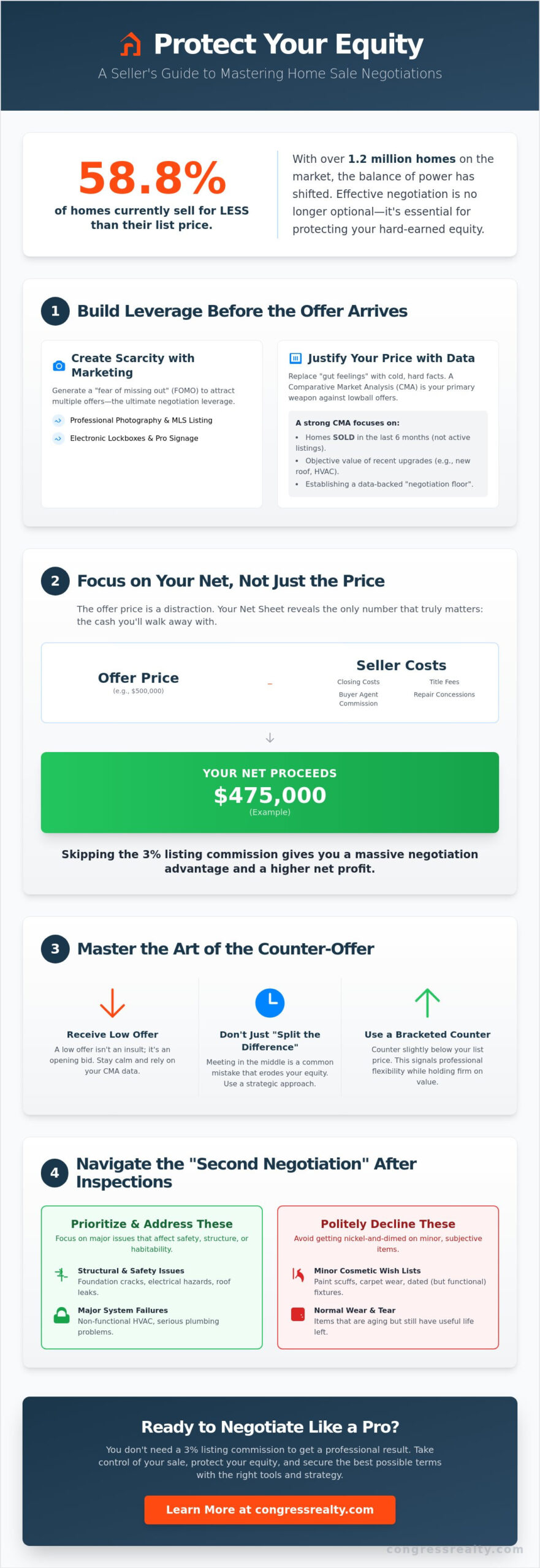

Did you know that 58.8% of homes are currently selling for less than their original list price? With inventory levels rising to over 1.2 million homes nationwide, the balance of power is shifting, making the skill of negotiating home sale price with buyers more critical than ever. It’s natural to feel a sense of dread when a lowball offer lands in your inbox or when a professional buyer’s agent pushes for aggressive concessions. You’ve worked hard to build equity, and the thought of losing it at the closing table is enough to keep any seller awake at night.

The good news is that you don’t need a traditional 3% listing commission to get a professional result. You can master the negotiation process while maintaining complete control over your transaction. This guide will empower you with the pragmatic tools needed to protect your proceeds and secure the best possible terms. We’ll break down exactly how to handle repairs, counter unfair offers, and use market data to move toward a successful closing with total confidence.

Key Takeaways

Ground your asking price in hard data with a Comparative Market Analysis (CMA) to build objective leverage before the first offer arrives.

Focus on your “Net Sheet” rather than just the top-line price to understand exactly how much you’ll keep after all concessions are calculated.

Master the art of negotiating home sale price with buyers by using bracketed counter-offers that show professional flexibility without caving on your equity.

Navigate the “second negotiation” after inspections by prioritizing structural and safety issues over minor cosmetic wish lists.

Use professional tools like electronic lockboxes and the MLS to maintain industry parity while enjoying the financial freedom of a fixed-cost listing.

Preparation: Building Your Negotiation Leverage Before the Offer

Leverage in real estate isn’t something you find; it’s something you build. Many sellers make the mistake of waiting for an offer to arrive before thinking about their strategy. True power in negotiating home sale price with buyers begins weeks before your home hits the market. It starts with replacing “gut feelings” with cold, hard data. When you walk into a transaction with a clear understanding of fundamental negotiation principles, you position yourself as a professional advocate for your own equity. You aren’t just a homeowner; you are the lead strategist in a high-value financial transaction.

The Role of the Comparative Market Analysis (CMA)

Your primary weapon for price justification is a professional Comparative Market Analysis (CMA). This document is the evidence you’ll use to shut down lowball offers before they gain momentum. To build a solid case, you must identify “true” comps. Look for homes that have sold within the last six months rather than focusing on active listings. Active prices represent what sellers hope to get, while sold prices represent what the market actually supports.

A detailed CMA also allows you to account for specific home improvements. If you’ve recently installed a new roof or upgraded your HVAC system, these aren’t just maintenance tasks. They are value-adders that provide a data-backed “no” to buyers trying to chip away at your price. Use this data to establish your “negotiation floor” so you never feel pressured to accept an unfair deal.

Creating Scarcity Through Marketing

High-end digital marketing and professional photography are non-negotiable tools for this. They drive traffic and increase the likelihood of multiple-offer scenarios, which is the ultimate leverage. When buyers see a listing that looks pristine and professional—the kind of high-quality presentation seen at Ray Lyon Realty—they perceive it as a high-demand asset.

Professional infrastructure also signals your seriousness as a seller. Utilizing tools like an electronic lockbox and a professional yard sign tells buyer’s agents that you are organized and prepared. This removes the “amateur” stigma often associated with independent selling and prevents professional agents from trying to out-maneuver you. By presenting a polished, professional front, you set the stage for a bidding war rather than a desperate hunt for a single buyer.

The relationship between listing price and sale price is a delicate balance. A strategic listing price, supported by your CMA, invites competition. When multiple buyers compete, the negotiation dynamic shifts entirely. You stop defending your price and start choosing the best terms from a position of strength.

Evaluating the Initial Offer: Separating Signal from Noise

Receiving your first offer is a major milestone, but don’t let the excitement cloud your financial judgment. The top-line price is often a distraction designed to capture your attention while hidden costs lurk in the fine print. Successful negotiating home sale price with buyers requires you to look past the sticker price and focus on the actual cash you’ll walk away with at closing. By adopting a methodical approach to offer evaluation, you can filter out weak proposals and focus on the deals that actually move the needle.

Calculating Your Net Proceeds

Your net proceeds are the only number that truly matters at the closing table. Net proceeds represent the final amount of cash you receive after all sale-related expenses, liens, and commissions have been deducted from the gross sale price. To find this figure, you must subtract closing costs, title fees, and buyer agent commissions from the total offer price. One of the most effective seller negotiation tactics is to maximize this number by controlling your expenses. When you skip the traditional 3% listing commission, you immediately increase your negotiation floor. This financial buffer allows you to be more flexible on the sale price while still netting more than a seller paying full-service fees. If you need help tracking these variables, using professional transaction management services ensures every dollar is accounted for accurately.

Vetting the Buyer’s Financials

A high offer price is worthless if the buyer can’t secure financing. In the 2026 market, you must distinguish between a pre-qualified buyer and one who is fully pre-approved. A pre-approval letter indicates that a lender has already verified the buyer’s income and assets, making the deal much more likely to close. If you receive an all-cash offer, you might consider accepting a slightly lower price in exchange for the certainty and speed it provides. Additionally, pay close attention to the earnest money deposit. A substantial deposit signals a buyer who is serious and has skin in the game, whereas a small deposit might indicate a lack of commitment.

Watch out for “red flag” contingencies that could jeopardize the sale later. While some contingencies are standard, excessive requests for home sale contingencies or unusual closing timelines can be deal-killers. If you encounter a lowball offer, don’t take it personally. Respond with a data-backed counter-offer based on your CMA. This keeps the conversation going and signals that you are a pragmatic seller who knows the market value of your property. By keeping your emotions in check and focusing on the data, you maintain the upper hand in every interaction.

The Art of the Counter-Offer: Moving Beyond the Sale Price

After you’ve vetted the buyer’s financials, it’s time to craft your response. Negotiation is a dialogue, not a zero-sum game. Start by acknowledging the offer and thanking the buyer. Maintaining a positive, professional tone prevents the transaction from becoming adversarial. This level of professionalism is a hallmark of expert representation, such as that provided by Robert Caicedo Real Estate. When negotiating home sale price with buyers, you should use a “bracketed” counter-offer. This involves meeting them partway between their offer and your list price. It demonstrates flexibility while signaling that you won’t accept a lowball figure. This approach keeps the buyer engaged while protecting your equity.

Momentum is your best friend in real estate. Always set a short expiration for your counter-offer, typically 24 to 48 hours. This creates a sense of urgency and prevents the buyer from “shopping” your offer to other sellers. Once you reach a verbal agreement, move quickly to get it in writing. Professional oversight ensures that every term you’ve fought for is accurately reflected in the contract. You’re in the driver’s seat, and setting these boundaries keeps the process moving toward your desired result.

Negotiating Terms vs. Dollars

Sometimes, the best way to protect your proceeds is to negotiate terms rather than the sale price. For example, an “As-Is” clause can be incredibly valuable. You might accept a slightly lower price in exchange for the buyer agreeing to take the property without any repair obligations. This eliminates the risk of expensive surprises later. Other powerful bargaining chips include flexible closing dates or seller leasebacks. A leaseback allows you to stay in your home for a set period after closing, which can save you thousands in temporary housing or double-moving costs. These non-monetary wins often provide more peace of mind than a few extra dollars in the sale price.

Handling Multiple Offers

If your marketing strategy has worked, you may find yourself juggling multiple contracts. This is the ultimate position of strength. Use a “Highest and Best” deadline to force buyers to put their most competitive terms forward simultaneously. When comparing these offers, look beyond the top-line number. An FHA loan might offer a high price but comes with stricter appraisal requirements and a 6% seller concession limit. A Conventional loan or a cash offer is often “cleaner” with fewer strings attached. Managing these moving parts requires precision. Utilizing professional transaction management ensures you don’t miss a deadline or a critical contingency while balancing multiple interested parties.

Handling Post-Inspection Negotiations and Concessions

Many sellers breathe a sigh of relief once a contract is signed, only to be blindsided by the inspection report. In the real estate industry, this period is often called the “second negotiation.” It’s the moment when buyers may try to claw back some of the sale price by highlighting every minor flaw in the property. Mastering the process of negotiating home sale price with buyers requires stamina during this phase. You must distinguish between legitimate safety hazards and a buyer’s “wish list” of upgrades. Your goal is to keep the deal on track without letting your equity bleed away through death by a thousand cuts.

Your original Comparative Market Analysis (CMA) remains your best defense here. If you priced the home accurately based on its current condition, you’ve already accounted for the age of the roof or the dated kitchen. Remind the buyer that the price they agreed to reflects the home as it stands. By staying grounded in the data you gathered during your preparation phase, you can push back against requests that aren’t rooted in structural or safety requirements.

Repair Credits vs. Physical Repairs

When an inspection reveals a valid issue, you generally have two choices: fix it yourself or offer a repair credit. Offering a credit is almost always the superior financial move for a seller. Credits are safer for sellers because they eliminate the risk of being held liable for “bad” repair work or delays caused by contractors. If a buyer presents an inflated estimate for a repair, don’t take it at face value. Get your own independent contractor quotes to challenge their numbers and keep the negotiation realistic. Cosmetic defects are typically not grounds for price renegotiation in a standard contract. Focusing strictly on “red flag” items like electrical hazards or foundation issues keeps the conversation professional and limited in scope.

The ‘Take It or Leave It’ Threshold

Before the inspection even begins, you should determine your “walk-away point.” This is the maximum amount you are willing to credit or spend before the deal no longer makes financial sense. Having this threshold in mind prevents emotional decision-making in the heat of the moment. You also need to be prepared for appraisal gaps. If the bank determines the house is worth less than the contract price, a new negotiation begins. You can ask the buyer to cover the difference, meet them in the middle, or stick to your price and risk the deal. If the buyer tries to walk away without a valid contractual reason, their earnest money deposit serves as your leverage. To ensure you have the professional support needed to handle these complex late-stage disputes, consider utilizing professional transaction management to protect your interests until the final signature is dry.

Navigating Negotiations Without a 3% Listing Commission

Negotiating home sale price with buyers becomes a lot less stressful when you aren’t starting from a 3% financial deficit. In a traditional model, you’re often pressured to hold out for a higher price just to cover the cost of the agent’s commission. When you remove that high-cost barrier, your “negotiation floor” drops significantly. This doesn’t mean you should accept less for your home. Instead, it means you have the financial breathing room to make strategic concessions that a commission-burdened seller simply cannot afford. You are in a position of unique competitive strength because your overhead is lower than almost every other listing on the block.

Congress Realty functions as your professional back-office support, providing the infrastructure you need to command respect in the marketplace. You maintain professional parity with every other listing by utilizing the Multiple Listing Service (MLS), professional photography, and an electronic lockbox. Buyers and their agents won’t see a “for sale by owner” amateur; they will see a serious, organized seller who has the same tools as a high-priced brokerage. This level of professional presentation is vital for negotiating home sale price with buyers because it prevents them from trying to exploit a perceived lack of experience.

The Flat Fee Competitive Advantage

Consider the math of a typical 2026 transaction. If you sell your home for $500,000 using a fixed-cost model, your net proceeds will likely be higher than if you sold that same home for $510,000 through a traditional agent charging a 3% listing fee. In that scenario, you’d be paying out $15,300 in listing commission alone. By choosing a smarter path, you can actually afford to be more flexible on your price to attract a wider pool of buyers while still keeping more of your equity. You aren’t just saving money; you are buying the flexibility to close deals faster.

Direct communication is your other secret weapon. When you are selling a house without an agent, you eliminate the middleman. You don’t have to wait for a listing agent to play “telephone” with the buyer’s agent. You hear the buyer’s concerns directly and can offer immediate, pragmatic solutions. This speed often keeps a deal alive when it might otherwise stall in a traditional communication chain.

Your Empowerment Checklist

Success in 2026 requires the right tools and a clear process. Use this checklist to ensure you are fully prepared to lead your own transaction:

Professional MLS Listing: Ensure your home is visible on the same databases used by every real estate professional.

Expert Valuation: Use a Comparative Market Analysis (CMA) to justify your price with hard evidence.

Professional Signage: Use a professional yard sign and post to signal a serious listing.

Transaction Management: Secure end-to-end oversight to ensure all legal paperwork is handled with precision.

Success in the 2026 housing market requires a shift from emotional reactions to a data-driven strategy. By grounding your listing in a professional CMA and focusing on your final net proceeds, you’ve already won half the battle. Master the art of negotiating home sale price with buyers by staying objective during inspections and using your lower overhead to out-position competing listings. You don’t need to pay a high-percentage commission to get professional results or maintain total control over your transaction. It’s about being the smartest person in the room, not the one with the most expensive agent.

Since 2002, Congress Realty has empowered thousands of savvy sellers to bypass traditional industry costs. Our fixed-cost fee structure ensures you know exactly what you’re paying upfront, while our Full Service Listing includes professional Transaction Management to handle the complex paperwork. You deserve a partner that provides the necessary infrastructure and then lets you lead the process with confidence. You’ve done the work to build your equity; now it’s time to keep it.

No, you aren’t obligated to accept the highest price offer. Often, a slightly lower offer with fewer contingencies, a flexible closing date, or all-cash financing is more valuable than a high-priced offer with risky strings attached. Evaluate the buyer’s financial strength and the speed of the transaction. Focus on your net proceeds and the likelihood of the deal closing without a hitch. The “best” offer is the one most likely to reach the closing table.

Can a buyer back out after we agree on a price?

Yes, a buyer can back out if they have active contingencies in the contract, such as inspection, financing, or appraisal clauses. These provide legal exits if specific conditions aren’t met. To minimize this risk, vet the buyer’s pre-approval letter and request a substantial earnest money deposit. Once all contingencies are waived, the buyer’s deposit is usually forfeited if they choose to walk away without cause. Professional transaction management helps track these critical deadlines.

How much should I counter-offer if the price is too low?

When negotiating home sale price with buyers, your counter-offer should be based on the hard data found in your Comparative Market Analysis (CMA). Avoid emotional reactions to lowball offers. Instead, use a “bracketed” approach by meeting the buyer partway between their offer and your list price. This signals professional flexibility while protecting your equity. Always justify your counter with specific market comps to keep the negotiation grounded in reality and professional logic.

Is it better to fix things before listing or offer a credit?

Offering a repair credit is generally better than performing the repairs yourself. Credits eliminate your liability for the quality of the work and prevent closing delays caused by contractor schedules. If you choose to fix items, focus only on structural or safety issues. Cosmetic defects are rarely worth the investment before a sale. Providing a credit lets the buyer handle the project to their own taste after closing while you move on.

What happens if the house appraises for less than the negotiated price?

If an appraisal comes in low, a new negotiation begins to bridge the appraisal gap. You can ask the buyer to pay the difference in cash, lower your sale price to the appraised value, or meet in the middle. If neither party can agree, the buyer can typically walk away with their earnest money. Use your CMA data to challenge a low appraisal if you believe the valuation is inaccurate based on recent local sales.

Do I still have to pay the buyer’s agent commission?

While the 2026 market offers more transparency, paying a buyer’s agent commission is still a common practice to attract the widest pool of buyers. However, this amount is entirely negotiable. By using a fixed-cost listing model, you save thousands on the listing side, which gives you more room to offer a competitive buyer’s agent fee without hurting your bottom line. Always define this fee clearly in your MLS listing to maintain professional parity.

How do I handle a buyer who wants to negotiate after the contract is signed?

Negotiations after a signed contract should only occur if new information comes to light, such as during the home inspection. If a buyer tries to renegotiate price without a valid contractual reason, stand your ground. Point back to the agreed-upon terms and your original market data. Utilizing professional transaction management can help you navigate these high-pressure moments and keep the buyer focused on the original agreement rather than looking for late-stage discounts.

What is the most important thing to include in a counter-offer?

The most critical element of a counter-offer is a short expiration deadline. Typically, giving a buyer 24 to 48 hours to respond maintains transaction momentum and prevents them from using your offer to shop for other properties. Clearly state your price, any adjusted contingencies, and the deadline. This firm boundary shows you are a serious, organized seller who values a swift and professional closing process. It forces the buyer to make a decision.