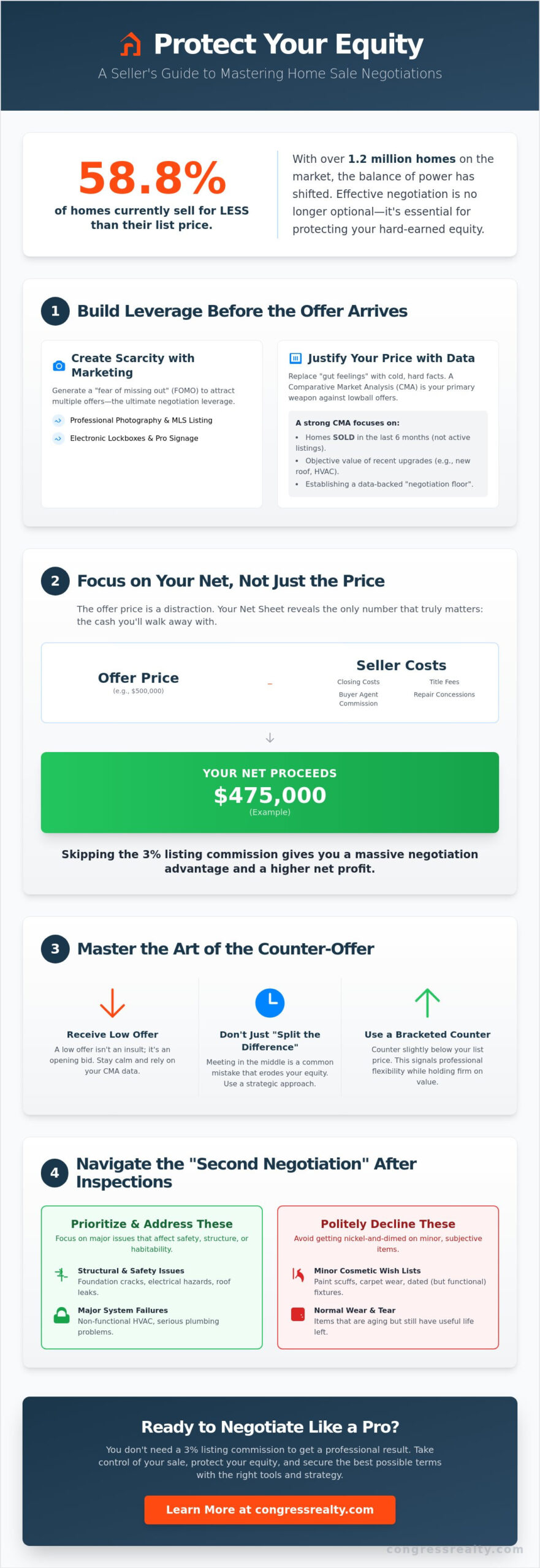

Did you know that 58.8% of homes are currently selling for less than their original list price? With inventory levels rising to over 1.2 million homes nationwide, the balance of power is shifting, making the skill of negotiating home sale price with buyers more critical than ever. It’s natural to feel a sense of dread when a lowball offer lands in your inbox or when a professional buyer’s agent pushes for aggressive concessions. You’ve worked hard to build equity, and the thought of losing it at the closing table is enough to keep any seller awake at night.

The good news is that you don’t need a traditional 3% listing commission to get a professional result. You can master the negotiation process while maintaining complete control over your transaction. This guide will empower you with the pragmatic tools needed to protect your proceeds and secure the best possible terms. We’ll break down exactly how to handle repairs, counter unfair offers, and use market data to move toward a successful closing with total confidence.

Key Takeaways

- Ground your asking price in hard data with a Comparative Market Analysis (CMA) to build objective leverage before the first offer arrives.

- Focus on your “Net Sheet” rather than just the top-line price to understand exactly how much you’ll keep after all concessions are calculated.

- Master the art of negotiating home sale price with buyers by using bracketed counter-offers that show professional flexibility without caving on your equity.

- Navigate the “second negotiation” after inspections by prioritizing structural and safety issues over minor cosmetic wish lists.

- Use professional tools like electronic lockboxes and the MLS to maintain industry parity while enjoying the financial freedom of a fixed-cost listing.

Preparation: Building Your Negotiation Leverage Before the Offer

Leverage in real estate isn’t something you find; it’s something you build. Many sellers make the mistake of waiting for an offer to arrive before thinking about their strategy. True power in negotiating home sale price with buyers begins weeks before your home hits the market. It starts with replacing “gut feelings” with cold, hard data. When you walk into a transaction with a clear understanding of fundamental negotiation principles, you position yourself as a professional advocate for your own equity. You aren’t just a homeowner; you are the lead strategist in a high-value financial transaction.

The Role of the Comparative Market Analysis (CMA)

Your primary weapon for price justification is a professional Comparative Market Analysis (CMA). This document is the evidence you’ll use to shut down lowball offers before they gain momentum. To build a solid case, you must identify “true” comps. Look for homes that have sold within the last six months rather than focusing on active listings. Active prices represent what sellers hope to get, while sold prices represent what the market actually supports.

A detailed CMA also allows you to account for specific home improvements. If you’ve recently installed a new roof or upgraded your HVAC system, these aren’t just maintenance tasks. They are value-adders that provide a data-backed “no” to buyers trying to chip away at your price. Use this data to establish your “negotiation floor” so you never feel pressured to accept an unfair deal.

Creating Scarcity Through Marketing

High-end digital marketing and professional photography are non-negotiable tools for this. They drive traffic and increase the likelihood of multiple-offer scenarios, which is the ultimate leverage. When buyers see a listing that looks pristine and professional—the kind of high-quality presentation seen at Ray Lyon Realty—they perceive it as a high-demand asset.

Professional infrastructure also signals your seriousness as a seller. Utilizing tools like an electronic lockbox and a professional yard sign tells buyer’s agents that you are organized and prepared. This removes the “amateur” stigma often associated with independent selling and prevents professional agents from trying to out-maneuver you. By presenting a polished, professional front, you set the stage for a bidding war rather than a desperate hunt for a single buyer.

The relationship between listing price and sale price is a delicate balance. A strategic listing price, supported by your CMA, invites competition. When multiple buyers compete, the negotiation dynamic shifts entirely. You stop defending your price and start choosing the best terms from a position of strength.

Evaluating the Initial Offer: Separating Signal from Noise

Receiving your first offer is a major milestone, but don’t let the excitement cloud your financial judgment. The top-line price is often a distraction designed to capture your attention while hidden costs lurk in the fine print. Successful negotiating home sale price with buyers requires you to look past the sticker price and focus on the actual cash you’ll walk away with at closing. By adopting a methodical approach to offer evaluation, you can filter out weak proposals and focus on the deals that actually move the needle.

Calculating Your Net Proceeds

Your net proceeds are the only number that truly matters at the closing table. Net proceeds represent the final amount of cash you receive after all sale-related expenses, liens, and commissions have been deducted from the gross sale price. To find this figure, you must subtract closing costs, title fees, and buyer agent commissions from the total offer price. One of the most effective seller negotiation tactics is to maximize this number by controlling your expenses. When you skip the traditional 3% listing commission, you immediately increase your negotiation floor. This financial buffer allows you to be more flexible on the sale price while still netting more than a seller paying full-service fees. If you need help tracking these variables, using professional transaction management services ensures every dollar is accounted for accurately.

Vetting the Buyer’s Financials

A high offer price is worthless if the buyer can’t secure financing. In the 2026 market, you must distinguish between a pre-qualified buyer and one who is fully pre-approved. A pre-approval letter indicates that a lender has already verified the buyer’s income and assets, making the deal much more likely to close. If you receive an all-cash offer, you might consider accepting a slightly lower price in exchange for the certainty and speed it provides. Additionally, pay close attention to the earnest money deposit. A substantial deposit signals a buyer who is serious and has skin in the game, whereas a small deposit might indicate a lack of commitment.

Watch out for “red flag” contingencies that could jeopardize the sale later. While some contingencies are standard, excessive requests for home sale contingencies or unusual closing timelines can be deal-killers. If you encounter a lowball offer, don’t take it personally. Respond with a data-backed counter-offer based on your CMA. This keeps the conversation going and signals that you are a pragmatic seller who knows the market value of your property. By keeping your emotions in check and focusing on the data, you maintain the upper hand in every interaction.

The Art of the Counter-Offer: Moving Beyond the Sale Price

After you’ve vetted the buyer’s financials, it’s time to craft your response. Negotiation is a dialogue, not a zero-sum game. Start by acknowledging the offer and thanking the buyer. Maintaining a positive, professional tone prevents the transaction from becoming adversarial. This level of professionalism is a hallmark of expert representation, such as that provided by Robert Caicedo Real Estate. When negotiating home sale price with buyers, you should use a “bracketed” counter-offer. This involves meeting them partway between their offer and your list price. It demonstrates flexibility while signaling that you won’t accept a lowball figure. This approach keeps the buyer engaged while protecting your equity.

Momentum is your best friend in real estate. Always set a short expiration for your counter-offer, typically 24 to 48 hours. This creates a sense of urgency and prevents the buyer from “shopping” your offer to other sellers. Once you reach a verbal agreement, move quickly to get it in writing. Professional oversight ensures that every term you’ve fought for is accurately reflected in the contract. You’re in the driver’s seat, and setting these boundaries keeps the process moving toward your desired result.

Negotiating Terms vs. Dollars

Sometimes, the best way to protect your proceeds is to negotiate terms rather than the sale price. For example, an “As-Is” clause can be incredibly valuable. You might accept a slightly lower price in exchange for the buyer agreeing to take the property without any repair obligations. This eliminates the risk of expensive surprises later. Other powerful bargaining chips include flexible closing dates or seller leasebacks. A leaseback allows you to stay in your home for a set period after closing, which can save you thousands in temporary housing or double-moving costs. These non-monetary wins often provide more peace of mind than a few extra dollars in the sale price.

Handling Multiple Offers

If your marketing strategy has worked, you may find yourself juggling multiple contracts. This is the ultimate position of strength. Use a “Highest and Best” deadline to force buyers to put their most competitive terms forward simultaneously. When comparing these offers, look beyond the top-line number. An FHA loan might offer a high price but comes with stricter appraisal requirements and a 6% seller concession limit. A Conventional loan or a cash offer is often “cleaner” with fewer strings attached. Managing these moving parts requires precision. Utilizing professional transaction management ensures you don’t miss a deadline or a critical contingency while balancing multiple interested parties.

Handling Post-Inspection Negotiations and Concessions

Many sellers breathe a sigh of relief once a contract is signed, only to be blindsided by the inspection report. In the real estate industry, this period is often called the “second negotiation.” It’s the moment when buyers may try to claw back some of the sale price by highlighting every minor flaw in the property. Mastering the process of negotiating home sale price with buyers requires stamina during this phase. You must distinguish between legitimate safety hazards and a buyer’s “wish list” of upgrades. Your goal is to keep the deal on track without letting your equity bleed away through death by a thousand cuts.

Your original Comparative Market Analysis (CMA) remains your best defense here. If you priced the home accurately based on its current condition, you’ve already accounted for the age of the roof or the dated kitchen. Remind the buyer that the price they agreed to reflects the home as it stands. By staying grounded in the data you gathered during your preparation phase, you can push back against requests that aren’t rooted in structural or safety requirements.

Repair Credits vs. Physical Repairs

When an inspection reveals a valid issue, you generally have two choices: fix it yourself or offer a repair credit. Offering a credit is almost always the superior financial move for a seller. Credits are safer for sellers because they eliminate the risk of being held liable for “bad” repair work or delays caused by contractors. If a buyer presents an inflated estimate for a repair, don’t take it at face value. Get your own independent contractor quotes to challenge their numbers and keep the negotiation realistic. Cosmetic defects are typically not grounds for price renegotiation in a standard contract. Focusing strictly on “red flag” items like electrical hazards or foundation issues keeps the conversation professional and limited in scope.

The ‘Take It or Leave It’ Threshold

Before the inspection even begins, you should determine your “walk-away point.” This is the maximum amount you are willing to credit or spend before the deal no longer makes financial sense. Having this threshold in mind prevents emotional decision-making in the heat of the moment. You also need to be prepared for appraisal gaps. If the bank determines the house is worth less than the contract price, a new negotiation begins. You can ask the buyer to cover the difference, meet them in the middle, or stick to your price and risk the deal. If the buyer tries to walk away without a valid contractual reason, their earnest money deposit serves as your leverage. To ensure you have the professional support needed to handle these complex late-stage disputes, consider utilizing professional transaction management to protect your interests until the final signature is dry.

Navigating Negotiations Without a 3% Listing Commission

Negotiating home sale price with buyers becomes a lot less stressful when you aren’t starting from a 3% financial deficit. In a traditional model, you’re often pressured to hold out for a higher price just to cover the cost of the agent’s commission. When you remove that high-cost barrier, your “negotiation floor” drops significantly. This doesn’t mean you should accept less for your home. Instead, it means you have the financial breathing room to make strategic concessions that a commission-burdened seller simply cannot afford. You are in a position of unique competitive strength because your overhead is lower than almost every other listing on the block.

Congress Realty functions as your professional back-office support, providing the infrastructure you need to command respect in the marketplace. You maintain professional parity with every other listing by utilizing the Multiple Listing Service (MLS), professional photography, and an electronic lockbox. Buyers and their agents won’t see a “for sale by owner” amateur; they will see a serious, organized seller who has the same tools as a high-priced brokerage. This level of professional presentation is vital for negotiating home sale price with buyers because it prevents them from trying to exploit a perceived lack of experience.

The Flat Fee Competitive Advantage

Consider the math of a typical 2026 transaction. If you sell your home for $500,000 using a fixed-cost model, your net proceeds will likely be higher than if you sold that same home for $510,000 through a traditional agent charging a 3% listing fee. In that scenario, you’d be paying out $15,300 in listing commission alone. By choosing a smarter path, you can actually afford to be more flexible on your price to attract a wider pool of buyers while still keeping more of your equity. You aren’t just saving money; you are buying the flexibility to close deals faster.

Direct communication is your other secret weapon. When you are selling a house without an agent, you eliminate the middleman. You don’t have to wait for a listing agent to play “telephone” with the buyer’s agent. You hear the buyer’s concerns directly and can offer immediate, pragmatic solutions. This speed often keeps a deal alive when it might otherwise stall in a traditional communication chain.

Your Empowerment Checklist

Success in 2026 requires the right tools and a clear process. Use this checklist to ensure you are fully prepared to lead your own transaction:

- Professional MLS Listing: Ensure your home is visible on the same databases used by every real estate professional.

- Expert Valuation: Use a Comparative Market Analysis (CMA) to justify your price with hard evidence.

- Professional Signage: Use a professional yard sign and post to signal a serious listing.

- Transaction Management: Secure end-to-end oversight to ensure all legal paperwork is handled with precision.

Ready to lead your own sale and protect your equity? Explore our Standard and Full Service listing packages today.

Secure Your Equity and Close with Confidence

Success in the 2026 housing market requires a shift from emotional reactions to a data-driven strategy. By grounding your listing in a professional CMA and focusing on your final net proceeds, you’ve already won half the battle. Master the art of negotiating home sale price with buyers by staying objective during inspections and using your lower overhead to out-position competing listings. You don’t need to pay a high-percentage commission to get professional results or maintain total control over your transaction. It’s about being the smartest person in the room, not the one with the most expensive agent.

Since 2002, Congress Realty has empowered thousands of savvy sellers to bypass traditional industry costs. Our fixed-cost fee structure ensures you know exactly what you’re paying upfront, while our Full Service Listing includes professional Transaction Management to handle the complex paperwork. You deserve a partner that provides the necessary infrastructure and then lets you lead the process with confidence. You’ve done the work to build your equity; now it’s time to keep it.

Take control of your equity with a Congress Realty Flat Fee MLS Listing today. Your path to a smooth, profitable closing starts here.

Frequently Asked Questions

Do I have to accept the highest price offer?

No, you aren’t obligated to accept the highest price offer. Often, a slightly lower offer with fewer contingencies, a flexible closing date, or all-cash financing is more valuable than a high-priced offer with risky strings attached. Evaluate the buyer’s financial strength and the speed of the transaction. Focus on your net proceeds and the likelihood of the deal closing without a hitch. The “best” offer is the one most likely to reach the closing table.

Can a buyer back out after we agree on a price?

Yes, a buyer can back out if they have active contingencies in the contract, such as inspection, financing, or appraisal clauses. These provide legal exits if specific conditions aren’t met. To minimize this risk, vet the buyer’s pre-approval letter and request a substantial earnest money deposit. Once all contingencies are waived, the buyer’s deposit is usually forfeited if they choose to walk away without cause. Professional transaction management helps track these critical deadlines.

How much should I counter-offer if the price is too low?

When negotiating home sale price with buyers, your counter-offer should be based on the hard data found in your Comparative Market Analysis (CMA). Avoid emotional reactions to lowball offers. Instead, use a “bracketed” approach by meeting the buyer partway between their offer and your list price. This signals professional flexibility while protecting your equity. Always justify your counter with specific market comps to keep the negotiation grounded in reality and professional logic.

Is it better to fix things before listing or offer a credit?

Offering a repair credit is generally better than performing the repairs yourself. Credits eliminate your liability for the quality of the work and prevent closing delays caused by contractor schedules. If you choose to fix items, focus only on structural or safety issues. Cosmetic defects are rarely worth the investment before a sale. Providing a credit lets the buyer handle the project to their own taste after closing while you move on.

What happens if the house appraises for less than the negotiated price?

If an appraisal comes in low, a new negotiation begins to bridge the appraisal gap. You can ask the buyer to pay the difference in cash, lower your sale price to the appraised value, or meet in the middle. If neither party can agree, the buyer can typically walk away with their earnest money. Use your CMA data to challenge a low appraisal if you believe the valuation is inaccurate based on recent local sales.

Do I still have to pay the buyer’s agent commission?

While the 2026 market offers more transparency, paying a buyer’s agent commission is still a common practice to attract the widest pool of buyers. However, this amount is entirely negotiable. By using a fixed-cost listing model, you save thousands on the listing side, which gives you more room to offer a competitive buyer’s agent fee without hurting your bottom line. Always define this fee clearly in your MLS listing to maintain professional parity.

How do I handle a buyer who wants to negotiate after the contract is signed?

Negotiations after a signed contract should only occur if new information comes to light, such as during the home inspection. If a buyer tries to renegotiate price without a valid contractual reason, stand your ground. Point back to the agreed-upon terms and your original market data. Utilizing professional transaction management can help you navigate these high-pressure moments and keep the buyer focused on the original agreement rather than looking for late-stage discounts.

What is the most important thing to include in a counter-offer?

The most critical element of a counter-offer is a short expiration deadline. Typically, giving a buyer 24 to 48 hours to respond maintains transaction momentum and prevents them from using your offer to shop for other properties. Clearly state your price, any adjusted contingencies, and the deadline. This firm boundary shows you are a serious, organized seller who values a swift and professional closing process. It forces the buyer to make a decision.